Understanding Equity Linked Saving Schemes (ELSS)

By Akhil Chugh

Date March 27, 2022

Tax planning is a very important aspect for success of any financial planning. There are various income tax saving schemes under which one can save their hard-earned money, ELSS or Equity Linked Saving Schemes, Insurance Policies and PPF or Public Provident Fund being the most popular ones. ELSS funds score over their traditional counterparts in terms of the superior tax efficiency of their returns, their comparatively shorter lock-in period, and their better odds of helping you create long-term wealth.

Let’s understand what are ELSS Mutual Funds and how investing in ELSS provides the dual benefit of wealth creation & tax saving.

What are ELSS Funds?

ELSS funds are the tax-saving mutual funds that invest the major portion of the investment corpus in equity and equity-related instruments. The fund manager based on his experience and knowledge picks securities of companies that have strong growth potential and a resilient business model.

ELSS funds offer a convenient way to avail tax advantage coupled with its ability to generate higher returns by harnessing the potential of the equity markets.

ELSS funds are also called tax-saving schemes as they offer tax exemption of up to Rs 1.5 lakh from your annual taxable income under Section 80C of the Income Tax Act.

Key Things to Know Before Investing in ELSS

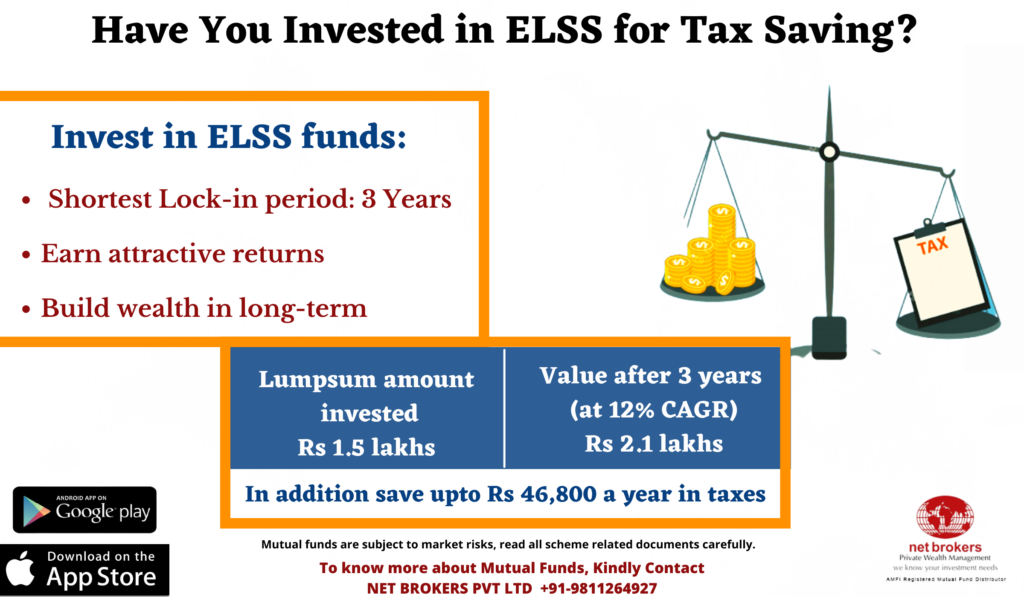

1. Shortest Lock-in Period:

ELSS has the shortest lock-in period among tax-saving investments under Section 80C of the Income Tax Act. You can invest and claim a tax deduction of up to Rs 1.5 lakh a year.

The Public Provident Fund or PPF has a lock-in period of 15 years. The other investment avenues like National Saving Certificates (NSC) have a minimum lock-in period of five years. The ELSS fund offers the shortest lock-in period, coupled with the possibility of higher returns.

However, you must decide on the investment amount, if you have invested in other tax-saving instruments under Section 80C. Invest in ELSS only if it matches your risk profile.

Also remember, in order to make the most out of ELSS investment, it is important to be patient and keep the fund invested for a longer time period.

2. Moderately high risk in nature:

ELSS funds, being an equity-oriented scheme, invest mostly in equity and equity-related securities. Equity funds carry a higher risk of fluctuation in Net Asset Value (NAV) as they are exposed to market volatility. Owing to this, ELSS funds may seem a risky proposition to some investors. However, this should not deter you from taking the benefit of such investments.

The trick here is to stay invested for a longer investment horizon. As compared to other asset classes, equity funds have been found to give above-average returns in the long run.

3. Gateway to equity investing:

ELSS is an equity-diversified mutual fund that invests primarily in stocks. It is an ideal way of investing in the stock market as you enjoy the benefits of diversification, professional management and tax saving!

Consider an investment in ELSS through a systematic investment plan or SIP. You can invest even Rs 500 a month, without timing the market. The slow and steady approach of investing through SIP imparts financial discipline.

Net Brokers believe that it is the ideal investment to get into the world of equity mutual fund schemes. Since these schemes come with a mandatory lock-in period of three years, investors would get used to the volatility typically associated with the stock market. Thus, giving them more confidence to start investing in other schemes.

4. Maximum Tax exemptions limits:

Under Section 80C, there is a limit to the amount of Rs 1.5 lakhs that you can claim for a tax deduction in a year. Another important point to keep in mind is that this deduction of Rs.1.5 lakhs is inclusive of other tax-saving investment options covered under Section 80C of the Income Tax Act. If you have investments in PPF for a sum of say, Rs 50,000, then the exemption on your ELSS funds would be Rs.1,00,000 only. So, do the calculations before finalising your investment amount. Remember, if you invest more than the required amount in ELSS, you won’t be able to claim an extra deduction under Section 80C.

5. Know the latest Tax implications:

The government of India has re-introduced the Long-Term Capital Gain (LTCG) tax at the rate of 10%, without any benefit of indexation to the investors. To protect the retail investors from higher tax incidence, long-term capital gain of Rs 1 lakh in a year will be tax-free. Only the gains above that will be taxed at 10% annually.

6. Availability of SIP option:

Avoid last-minute hasty investments, and start investing for saving tax and other financial goals at the beginning of the financial year. Choose the Systematic Investment Plan (SIP) for regular investments in equities for greater compounding benefits over an extended period. The advantage of rupee cost averaging allows you to purchase more stocks when the market is down and sell the same in case of market rise apart from inculcating financial discipline.

7. Avoid investing in too many ELSS funds:

It’s tempting for investors to invest in a new fund each year and then end up with 7-8 funds in their portfolio. Multiple investments are tough to track. This leads to a portfolio over-diversification which may hurt your returns over the long term. Not only that, but having too many ELSS funds will also make it difficult for you to track their performance diligently and leave you with no control over your investments. Ideally one should have around 1-2 top-performing ELSS funds in their portfolio. You should then track their performance periodically.

Net Brokers Takeaways:

- Net Brokers believes that ELSS is one of the best tax-saving tools available to an investor to get the twin benefit of tax savings and an opportunity to harness the potential upside of investing in the equity market.

- One should carefully scrutinize various ELSS schemes before making investments. Gauge your risk appetite and the time horizon for which you can stay invested to choose the fund that best suits your investment goals.

- Taxation plays an integral role in overall financial planning; hence Net Brokers strongly suggest investors plan their investments in ELSS systematically at the starting of the year and not towards the end of the fiscal. One can start looking at investing in an ELSS scheme through SIP to benefit from rupee cost averaging to beat market volatility and avail tax benefit up to Rs.1.5 lakhs for a year as per the current tax laws.

- Equity markets can be volatile in the short term and therefore, investors should be patient and have a sufficiently long investment horizon for Equity Linked Savings Schemes (ELSS). Though the lock-in period for ELSS investments is 3 years, an investor should be willing to stay invested for a minimum horizon of 7-10 years to earn higher returns.

Equity Linked Savings Schemes are one of the best Section 80C investment options to avail tax deduction. Invest smart with Net Brokers Mutual Fund App in the right ELSS fund and start a monthly SIP in an ELSS fund to get triple benefits – tax savings, systematic investing, and an opportunity to harness the potential upside of investing in the equity market.

For more information, get in touch with us today! Download our mutual fund app & start investing in an ELSS fund to save tax and grow your capital significantly over the long term.

Happy Tax Saving!