Late to Investing? Here Are 5 Things You Can Do

Many people believe they are “too late” to start investing. Maybe you spent your 20s focusing on career growth.

Maybe responsibilities delayed your financial planning.

Or maybe investing always felt confusing and overwhelming.

The truth is, while starting early is beneficial, starting late is far better than not starting at all.

If you feel behind on your investment journey, here are five practical steps you can take today.

Get Clear on Your Financial Goals:

Before worrying about returns, first define your destination. Ask yourself:

![]() What am I investing for? (Retirement, children’s education, home purchase?)

What am I investing for? (Retirement, children’s education, home purchase?)

![]() How many years do I have?

How many years do I have?

![]() What level of risk can I realistically

What level of risk can I realistically

handle?

Clarity brings structure. When goals are defined, investment decisions become logical instead of emotional.

If someone wants ₹1 lakh per month in retirement income, for 25 years after retirement, assuming 6% inflation, they may need approx ₹3–4 crore corpus at retirement (depending on return assumptions).

Now reverse calculate:

If you are 40 years old and want ₹3 crore by age 60 (20 years): At 12% CAGR, you need to invest ₹₹33,050 per month.

Even if you’re starting late, a focused

and goal-based strategy

can help you catch up systematically.

Increase Your Investment Amount Gradually

If time is limited, contribution becomes more important.

Since compounding has less time to work, you can compensate by:

- Increasing your SIP amount.

- Allocating bonuses or increments toward investments.

- Avoiding lifestyle inflation.

Small increases every year can significantly improve long-term outcomes.

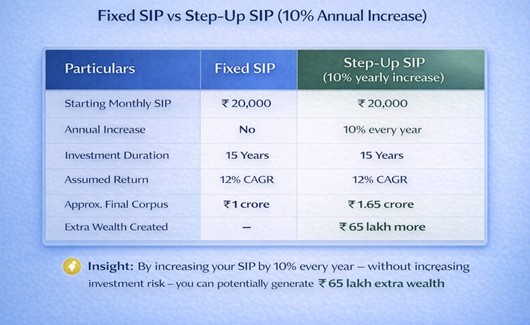

Suppose someone invests:

₹20,000 per month for 15 years at 12% CAGR

→ Corpus ≈ ₹1 crore

Now, if they increase SIP by 10% every year (step-up SIP):

₹20,000 starting SIP 10% annual increase

15 years at 12% CAGR

→ Corpus ≈ ₹1.65 crore

That’s nearly ₹65 lakh extra, without chasing higher returns.

Remember, consistency matters more than timing.

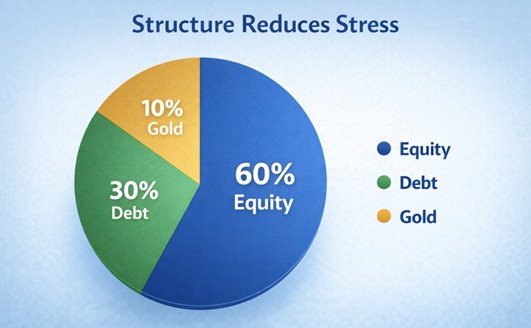

Choose the Right Asset Allocation

Historical data shows:

- Equity markets can correct 20–30% in a year.

- Balanced Advantage / Hybrid funds historically show lower volatility compared to pure equity.

- Long-term equity CAGR in India (15+ years) has ranged around 11–14% depending on the index and time period.

When starting late, asset allocation becomes crucial.

A balanced mix of equity (for growth), debt (for stability), and Gold or other assets (for diversification, if suitable) can help manage risk while aiming for reasonable growth.

Avoid the temptation to take excessive risk just to “catch up.” Aggressive decisions often create setbacks instead of progress.

Avoid High-Cost Debt Before Aggressive Investing

If you’re carrying high-interest loans (like credit card debt or personal loans), prioritise clearing them.

Why?

Because:

- The interest you pay may be higher than potential investment returns.

- Debt reduces financial flexibility.

- Emotional stress from debt impacts long-term planning.

₹5 lakh credit card debt Interest @ 36% per annum

After 1 year unpaid → becomes approx ₹6.8–7 lakh.

Compare with mutual fund return:

If ₹5 lakh invested at 12% CAGR → becomes ₹5.6 lakh

The difference is massive.

Building a strong foundation improves investment confidence.

Stay Disciplined

It’s easy to compare yourself with peers who started investing early.

But financial journeys are personal. Focus on your income growth, your savings rate, and your long-term consistency.

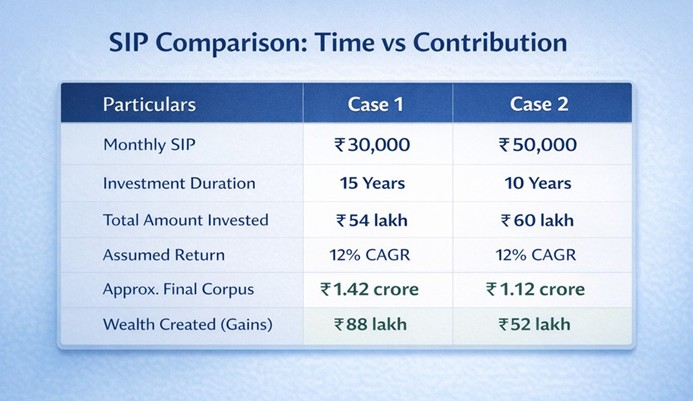

Suppose, Case 1:

₹30,000 SIP 12% CAGR

15 years

54 lakhs invested

→ ₹1.42 crore approx

Case 2:

₹50,000 SIP 12% CAGR

10 years

60 lakhs invested

→ ₹1.12 crore approx

Time in the market and discipline play a critical role in compounding.

If you’re starting late, you may need to increase your contribution. But if you still have time on your side, consistency over a longer period can create substantial wealth, even with moderate investments.

What Should You Remember?

Starting late does not mean starting wrong.

It simply means your strategy needs to be intentional.

- Be clear about goals.

- Invest consistently.

- Increase contributions when possible.

- Avoid emotional decisions.

- Review periodically.

Markets reward discipline more than perfect timing.

The Money Monday Perspective

The best time to start investing was yesterday. The second-best time is today.

Regret does not build wealth. Action does.

No matter your age or stage, a structured plan, diversification, and patience can help you move closer to financial freedom.

Conclusion:

If you feel late to investing, don’t let that delay you further. Every year you wait reduces opportunity but every year you invest builds momentum. Wealth creation is not about when you start alone; it’s about how consistently you stay invested.

Start where you are. Invest with clarity.

Let time do its work.