Investing in Mutual Funds: SIP vs Lump Sum

By Akhil Chugh

Date September 4, 2021

Investing in mutual funds is a great investment approach to build wealth, as it allows you to gain exposure to a number of assets depending on the type of mutual fund it is. There exist many types of mutual funds, such as equity funds that invest primarily in stocks, debt funds that focused on fixed income instruments, and balanced funds that are a mixture of the two. You can invest in mutual funds either through a large one-time payment known as a lump-sum investment or through a SIP.

In this article, we will provide a breakdown of the two types of investment methods, along with the benefits of each strategy so that potential investors can make better, more informed investment decisions while investing in mutual funds.

What is SIP?

SIP is a disciplined form of investing allowing you to invest money into a mutual fund scheme periodically, such as daily, weekly, monthly, quarterly, or half-yearly, etc.

In this case, a fixed amount gets deducted automatically from your bank account and is invested into the mutual fund schemes you have chosen every month on a predetermined date.

How SIP Works?

The concept of SIP is quite simple – you start by first determining the amount of money you want to save and invest every month. The second step involves choosing the desired funds for investing. If you are unsure, you can download the Net Brokers app to know which risk profile you belong to and accordingly pick mutual funds from the list given as per your financial goals.

Every time you invest money, additional units of the mutual fund scheme are brought at the market rate and added to your account. Thus, you keep buying units at different rates – more units when the market is low & fewer units when the market is high – helping investors to benefit from rupee cost averaging as well as the power of compounding.

Pros of Investing in Mutual Funds via SIP

1. Financial discipline:

The golden rule to build a corpus of wealth, in the long run, is to invest regularly, stay focused and maintain discipline. SIPs can get investors into the habit of saving frequently thus inculcating financial discipline.

-

Timing the market becomes irrelevant:

The main benefit of SIP is that you don’t have to time the market. Since you are entering the market during different market cycles, investors do not have to watch the market movements as closely as they would have to for lump sum investments.

-

Rupee cost averaging:

With SIP, an investor is purchasing mutual fund units during different market cycles, the cost per unit is averaged out over the overall investment horizon. More number of units are purchased during a market low compensating for the low number of units purchased during a market high. Thus, averaging out the total purchase cost for mutual fund investors helping them to tide over the market volatility.

-

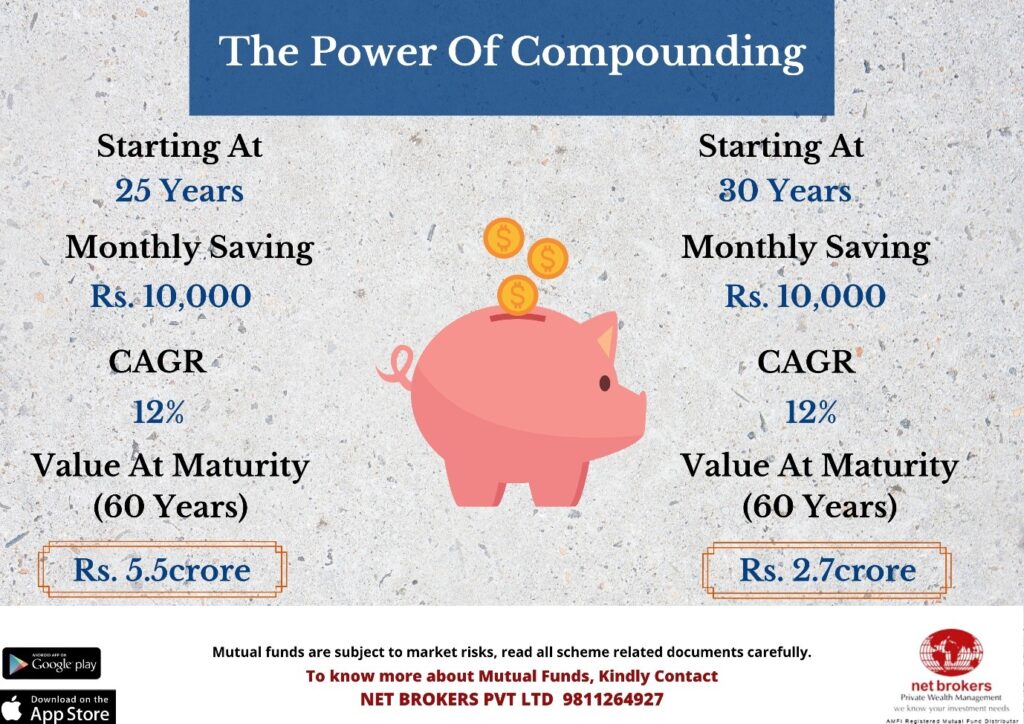

Power of compounding:

When you invest via SIP, the interest earned on your investment is reinvested which means your returns themselves start earning interest. Hence, the compounding effect helps generate greater returns. To garner the benefit of the power of compounding, it is always advisable to start investing early.

Let’s look at an example below for a better understanding of this concept,

As is evident from the above illustration, a delay of 5 years which is Rs 6 lakhs difference in the invested amount led to the difference of over 2.5 crores in the total corpus at their respective age of retirement.

5. Less stressful:

SIP investments are less stressful, hence making them an ideal choice for novice investors. Market volatility can sometimes make you panic and withdraw your money for fear of further loss in case of lump-sum investment. This is less intense in the case of SIP because the money invested is spread across time.

What is Lump Sum Investment?

A lump sum investment is a one-time large sum of money invested in any given mutual fund scheme.

Let’s take, for example, an individual who has a large amount of money after making a windfall gain or has received the amount from their PF fund, and wishes to invest it in mutual funds. One of the ways they could achieve this is by investing the whole amount in one mutual fund at one time. This would be known as a lump sum investment.

How Lump Sum Investment Works?

1. A bullet investment:

Define an asset allocation, choose suitable funds and invest in them all at once!

This is particularly risky. If you end up investing at a very high market valuation, your investment could be subjected to volatility that you may not be very comfortable with.

-

STP – Systematic Transfer Plan:

STP is a cousin of SIP.

In a SIP, the money is invested into a set of funds at regular intervals. The source of the money is your bank account.

In an STP, the same thing happens with one difference. You don’t invest from your bank account, you invest from a low-risk fund.

For example – Let’s say your lumpsum investment amount is Rs. 20,00,000. If you choose the STP mode, you will choose a liquid fund firstly and invest all the amount in the liquid fund. From this liquid fund, you can start an STP into an equity fund over a certain period. Let’s say this is 20 months. What will happen is that Rs. 100,000 will be transferred from the liquid fund to the equity fund every month for 20 months.

The lump sum in a liquid fund will fetch you higher returns than saving bank interest and at the same time, will allow the averaging by entering the market systematically. This strategy acts as a defence against market volatility.

Pros of Investing via Lump Sum Mode:

- Ease of investing at once without any further commitment to future investments

- Suitable for investors with lump sum amount of money to invest

- If you’ve been tracking the market for a while, and can predict its growth with near certainty, then a lumpsum investment is likely to net you higher absolute over investing small amounts regularly through a SIP which tends to give a weighted average return over the long-run.

Net Brokers Takeaways:

- It should never be a SIP vs Lump sum. There is always an ‘and’ in between them as they go hand in hand. An investor cannot alone choose one type of investing option to create wealth. Lump sum or SIP in mutual fund investing have their own benefits and work for different investors at different times.

- If you have a considerable amount of investible surplus and want to make a lump sum payment one-time, lump sum investment is the ideal choice. However, you should carefully time the market for investing at the right time to get the maximum returns on your investment.

- Your cash flow should be the most important factor in your choice of investment vehicle. If you have a regular investible surplus, use the SIP route. But if you have got a one-time windfall – for example, a bonus or proceeds from a sale – invest as a lump sum. Even when you are investing in a lump sum, you can minimize your risk by parking your funds in a safe debt fund and use the STP (systematic transfer plan from one mutual fund scheme to another) to move it to equity funds over time.

- Net Brokers believes that SIPs are superior on two counts: they can help you tide over market fluctuations and be a good investment option even for novice investors since they do not necessitate frequent monitoring of financial markets.

- Based on factors like investment amount and experience, you need to decide which type of investment is more suitable for you. You can also use a strategy to use a combination of both SIP and lump sum to maximize your returns.

Net Brokers recommend investors to keep SIP as the core strategy in your portfolio but if you have an investible surplus or a windfall earning, you can invest it as a lump sum in debt funds and opt for the STP route to move it to equity funds over a time period.

For more information, get in touch with us today! Download our mutual fund app & start investing for your long-term financial goals.

Happy investing!