How are Mutual Funds Taxed?

By Akhil Chugh

Date April 24, 2022

Mutual Funds are one of the best available investment avenues to help you create wealth and achieve all your financial goals. Mutual Funds are also tax-efficient instruments compared to its alternatives like Fixed deposits wherein the interest earned is added to your taxable income and taxed at your income tax slab rate. This is where Mutual Funds fare better.

In this blog, let’s look at the key elements of Mutual Funds taxation to help you plan your investments to minimize your overall tax outgo.

Key Factors Determining the Mutual Funds Taxation in India:

1. Type of Mutual Fund:

There is a variety of Mutual Funds available in the market for different types of investors based on the risk appetite and investment goals. Taxation on Mutual Funds depends on what type of funds you have invested in. For taxation purposes, Mutual Funds are divided into 2 main categories: Equity Funds and Debt Funds.

Mutual Funds that invest more than 65 percent of their portfolio in domestic company equities is categorized as an equity-oriented fund for taxation purposes.

A debt fund (i.e., a non-equity-oriented fund) that invests in different fixed-income securities carries a different tax rate from equity-oriented funds. International funds investing in stocks abroad, and fund-of-funds that make money through investments in various Mutual Funds are taxed like debt funds.

Hybrid funds are treated as equity-oriented funds only if they have a minimum of 65 percent exposure to domestic company equities. Otherwise, they are treated as debt funds.

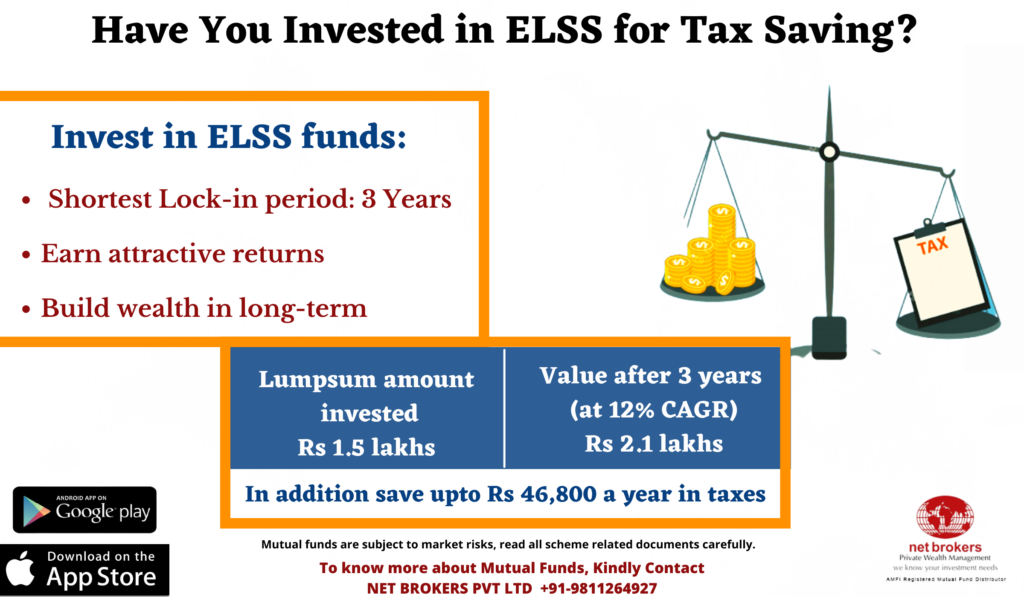

ELSS mutual funds, though primarily invested in the stock market, are tax-saving mutual funds. What sets ELSS apart from other equity-oriented funds is the minimum lock-in period of three years.

2. Type of Returns Generated

Mutual Funds offer investors returns in two forms – Dividends and Capital Gains.

Dividends are paid out of the profits of the company. When the companies are left with surplus cash after meeting all their expenses, they may decide to share the same with investors in the form of dividends. Investors receive dividends proportional to the number of mutual fund units held by them. The entire dividend income is taxable in the hands of the investor as per the income tax slab under the head “income from other sources.”

On the other hand, Capital Gain is the profit realized by investors if the selling price of the security held by them is greater than the purchase price. Capital Gains are realized on the sale of mutual fund units. For example, if you hold units of a mutual fund scheme that you purchased when the NAV was ₹200, you will generate a capital gain when the price moves above ₹200, and you sell the units. It is only at the time of redemption that the mutual fund capital gain tax accrues.

3. Holding Period:

The duration for which you hold on to your mutual fund investment is called the holding period. The holding period decides the rate of tax you’ll pay on your capital gains. The greater your holding period, the less tax you’ll pay.

a. Short-term taxation

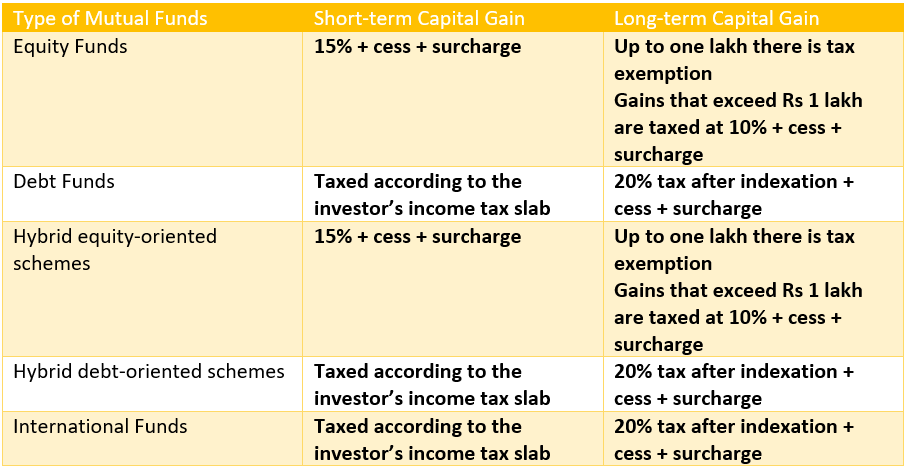

Investment in any equity-oriented mutual fund for less than 12 months is considered short-term and attracts a short-term capital gains tax of 15 percent.

For debt funds, a holding period of less than 36 months is considered a short-term investment. Short-term capital gains on debt funds are taxed according to your income slab.

b. Long-term taxation

Gains from equity mutual funds held for more than 12 months attract long-term capital gains tax at 10 percent if the total long-term capital gains amount from equity-oriented mutual funds/ equity shares exceeds ₹1,00,000 in a year. Returns below that threshold are tax-free.

Gains from debt funds, on the other hand, are taxed at 20 percent after indexation benefit, if held for over 36 months. Indexation refers to gains adjusted for inflation. Without indexation, the tax on debt funds would be higher.

Note: When you invest in an ELSS fund, you are eligible for a tax deduction. You can save up to ₹1,50,000 under Section 80C of the Income Tax Act, 1961. Although primarily an equity fund, the lock-in period of three years and the high probability of return generated makes it one of the best tax saving options available to investors.

Snapshot: Taxation on Mutual Funds

Net Brokers Takeaways:

- Mutual fund investments done for a longer period are tax-efficient. Plan your investments for a longer tenure to enjoy the benefit of lower taxation and the power of compounding.

- Investments up to Rs 1.5 lakh Equity Linked Savings Schemes (ELSS) are eligible for deduction u/s 80C subject to a 3-year lock-in period.

- In the case of SIP, tax is calculated for each unit. The holding period from the date of purchase to the redemption date determines whether it will be considered for short-term or long-term capital gains tax. If redemption is carried out in parts, then the first-in, first-out rule is applied, meaning that the first units purchased are considered sold first.

Mutual Funds can help you reach your financial goals with careful planning. Holding funds for the long haul makes them more tax-efficient. Always account for tax when you calculate your returns. In case of any query, feel free to contact us.

Happy investing!