How does SIP Top-up work?

The SIP Top-up amount can be either a specific percentage of your original SIP amount or even a predetermined fixed amount. The frequency of increasing the amount is typically half-yearly or annual.

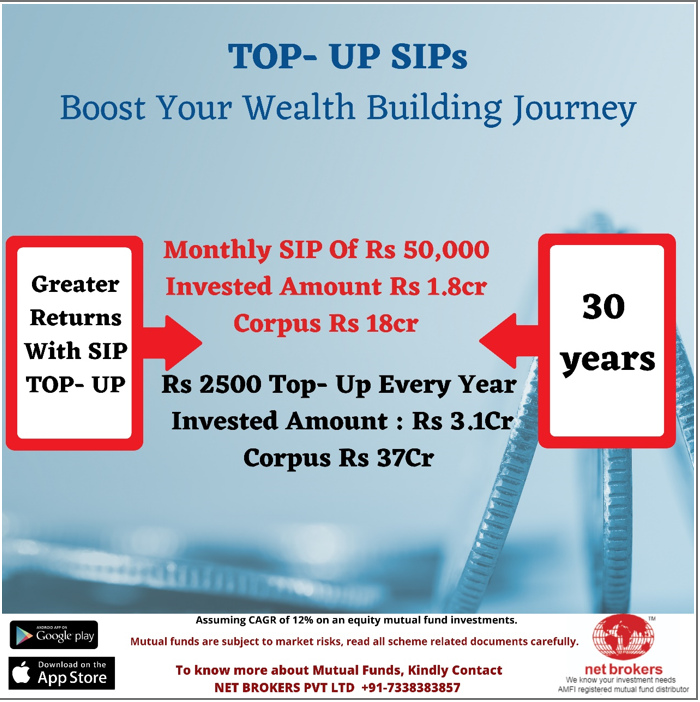

Let us assume that you have a monthly SIP of Rs 25,000 in a mutual fund scheme. If you opt for a Rs 1,000 SIP top-up on an annual basis, your monthly SIP instalments will be Rs 26,000 after one year and Rs 27,000 in the following year. If you opt for a 10% SIP top-up on an annual basis, your monthly SIP instalments will be Rs 27,500 after one year and Rs 30,250 in the following year.

Thus, under the step-up SIP scheme, your SIP amount would increase by a specified amount every year, allowing you to step up your investments over time. You can also specify a maximum SIP amount, which would serve as the maximum limit to which the SIP would increase over time. When the increased SIP reaches the maximum specified amount, no more increase would be affected, and your investments would continue at the maximum amount.

A top-up facility lets the investor accelerate the timeline to reach the target corpus.

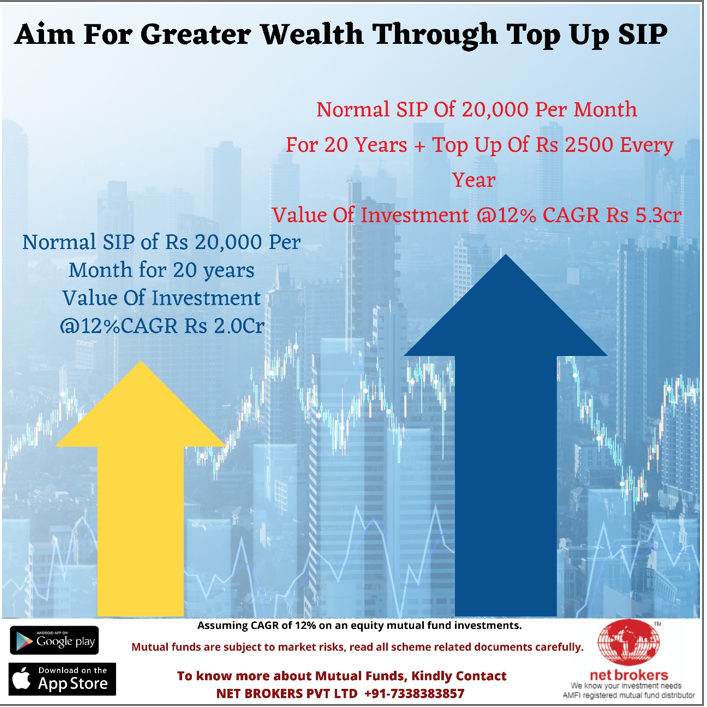

Traditional monthly SIPs vs SIP Top-ups:

Suppose, Mr. Ranbir wants to save money for his retirement home in 20 years. He decides to start a SIP in a chosen mutual fund scheme. By investing Rs 20,000 each month and assuming a return of 12% p.a., he reaches a corpus amount of Rs 2.0cr in 20 years.

On the other hand, if he starts his SIP of Rs 20,000 in the same mutual fund scheme but with a commitment to top up his SIP amount by Rs 2500 every year, he would be able to accumulate a corpus amount of Rs 5.3cr in the same time period of 20 years.

Now, with larger corpus Ranbir can afford to buy a larger retirement home and lead a comfortable retirement life by opting for a SIP Top-up to achieve his goals.