A Bulletproof Guide to Child Education Planning

By Akhil Chugh

Date October 8, 2023

“An investment in knowledge pays the best interest” – Benjamin Franklin

Education serves as the cornerstone of a child’s future security. While every parent aspires to provide the finest education for their children, the escalating costs pose a significant concern. The expenses associated with higher education have surged in recent years, surpassing the inflation rate by a considerable margin.

For instance, consider the fees for a PGP course at IIM Ahmedabad, which stood at Rs 11.5 lakhs in 2008 and has now soared to Rs 23 lakhs. Similarly, the fees for an IIT B.Tech program amounted to Rs 2.28 lakhs in 2008 but has escalated to Rs 10 lakhs today.

For students aiming to pursue education in foreign universities, the costs are nearly four times higher, excluding additional expenses such as accommodation and travel.

In the present era, sending your child to college necessitates meticulous planning, strategic investment in the right financial instruments, and the establishment of a well-structured timeline. Regular review and recalibration are also vital components of this process. Achieving this goal requires a forward-thinking and comprehensive plan.

Planning for your child’s education is a vital milestone in shaping their future, and it requires careful consideration and preparation to ensure their success.

7 Mistakes to Avoid While Planning for Your Child’s Education

In this section, we’ll provide you with a comprehensive and “bulletproof” guide to your child’s education planning. By following these steps, you can ensure that your child has the best opportunities to succeed without breaking the bank.

1. Lack of Early Planning:

Mistake: It is common for parents to get complacent and delay the investment process thinking there is ample time to invest. In the gamut of investments, time plays an extremely crucial role – the sooner you start saving and investing, the more time you will have for the power of compounding to allow it to work its magic on your money. It is very important to start early for success of child education planning.

Solution: Start a SIP early to benefit from the power of compounding. The longer your investments grow, the less financial burden you’ll face when your child enters college.

For example, if your child is currently 4 years old and currently the cost of higher education (Grad+post-grad) is Rs 50,00,000. Then the future cost of same education assuming 7% inflation rate will be Rs 1.5cr. If you start investing today then the monthly SIP required to achieve the target is Rs 35,857 considering the expected CAGR of 12%.

However, if you delay your investments by 5 years or 10 years you will have to invest Rs. 56,048 or Rs. 1,23,544/month respectively.

But if you start investing when the kid is 1 year old, the required monthly SIP would only be Rs 29,108.

2. Insufficient Goal Estimation:

Mistake: Underestimating the cost of education.

Solution: Over the years, education costs have escalated quite a bit. Use SIP calculators to determine the required monthly investment amount based on your child’s future education expenses. Make sure you consider inflation in your calculations. According to rough estimates, on an annual basis the education inflation is about 10 percent p.a.

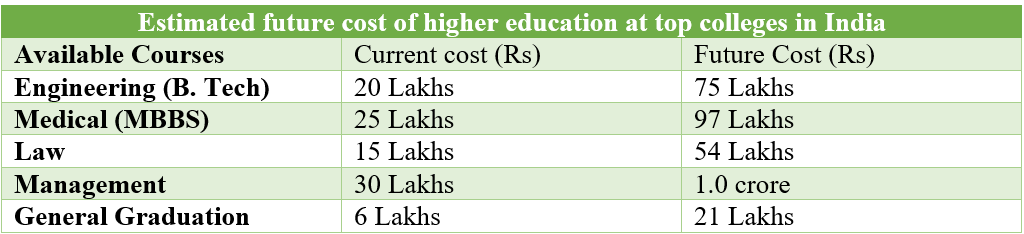

To estimate the size of the investment corpus required, let’s look at the cost of some popular courses in India at top institutes and assess their future cost 18 years from now, assuming the conservative inflation rate at 7% p.a.

Even by conservative estimate, if education cost inflation of 7 per cent a year is considered, then a 4-year engineering course that costs Rs 20 lakh at present will cost around Rs 75 lakh after 18 years. Similarly, a 2-year MBA course that costs around Rs 30 lakhs would cost around Rs 1.0 crore over the same time period. Here, we have considered the course fees for top colleges in India. The cost would be significantly higher (almost 4 times) if your education plan includes studying at a reputed foreign university.

Knowing the required corpus to finance your child’s higher education will help you understand the amount of savings that are required to be invested for child’s higher education. Hence it is crucial to figure out a realistic number and design an investment plan accordingly to ensure that you do not fall short of funds for your child’s education.

3. Neglecting Diversification:

Mistake: Over-reliance on a single investment or asset class.

Solution: Never invest in assured but low-return investment products/insurance policies. Don’t play it safe when it comes to planning over a 15-year period. Diversify your investments across mutual funds with varying asset allocations (equity, debt, hybrid). SIPs in diversified mutual funds spread risk and offer long-term growth potential.

Equity funds are best suited to outperform over the long term. Net Brokers believe that if you have a 15-year time frame there is no point in putting a lot of money in debt. Look at investing at least 80% of your money in equity funds to earn inflation-beating returns. If you invest too much in debt, you are limiting your return-generating capacity.

4. Ignoring Risk Tolerance:

Mistake: Choosing investments without considering your risk tolerance.

Solution: Select mutual funds aligned with your risk appetite. Aggressive investors can opt for equity-oriented SIPs, while conservative investors can choose debt or balanced funds.

5. Not Staying Informed:

Mistake: Neglecting to monitor your investments.

Solution: Regularly review your mutual fund portfolio’s performance and make adjustments if necessary. SIPs provide the flexibility to increase or decrease your investments based on market conditions.

Net Brokers suggest keeping your investments dynamic and tweaking the equity / debt mix as you go along. When you have 15 years to your child’s education it is fine to remain 80% in equities but not when the milestone is just 2 years away.

6. Skipping Emergency Fund:

Mistake: Not having a financial safety net.

Solution: Before starting SIPs for your child’s education, establish an emergency fund to cover unexpected expenses. This ensures you won’t have to dip into your education corpus prematurely.

7. Overlooking Tax Efficiency:

Mistake: Not optimizing tax benefits.

Solution: Invest in tax-efficient mutual funds like Equity Linked Savings Schemes (ELSS) that offer tax deductions under Section 80C of the Income Tax Act. SIPs in ELSS help you save on taxes while accumulating wealth.

Net Brokers Takeaways:

- Consider a Higher Inflation Rate: To safeguard your child’s future, it’s wise to plan for a higher level of inflation, ideally in the range of 7% to 10%. Avoid assuming lower inflation rates that may not reflect reality.

- Start your child’s education planning as early as possible and allocate the right amount of funds to the right investment products. Utilize the Net Brokers app and leverage our Child Education Calculator to determine the future cost of your dream education.

- Avoid making lump-sum investments and instead opt for SIPs. This strategy allows you to benefit from rupee cost averaging over the long term, reducing the impact of market volatility.

- Consider increasing your SIP investments incrementally as your income rises. This approach can help you either use the funds for other purposes or expedite the growth of your education corpus.

With a multitude of investment options in the market, it’s easy to feel overwhelmed. To make informed decisions and optimize your investments according to your risk tolerance and goals, consider seeking assistance from Net Brokers. We can help you select the most suitable investment solution to match your financial objectives.

By keeping these strategies in mind, you can proactively plan for your child’s education, mitigate inflationary pressures, and make well-informed investment choices to secure their future. Don’t hesitate to reach out to Net Brokers for personalized guidance tailored to your unique financial situation.

Take the right step at the right time to make your child’s dream come true.

For more information, get in touch with us today! Download our mutual fund app & start investing for your long-term financial goals.

Happy investing!