Planning For Your Child’s Future

By Akhil Chugh

Date June 19, 2021

‘Education is the Key to Unlock the Golden door Of Freedom.’ – George Washington Carver

Education is the foundation stone for a child’s future security. However, while every parent wants to provide their child with the best of available education opportunities, the costs are a major concern. The cost of higher education has gone up considerably in last few years. Higher Education costs are rising at a rate significantly higher than the inflation rate.

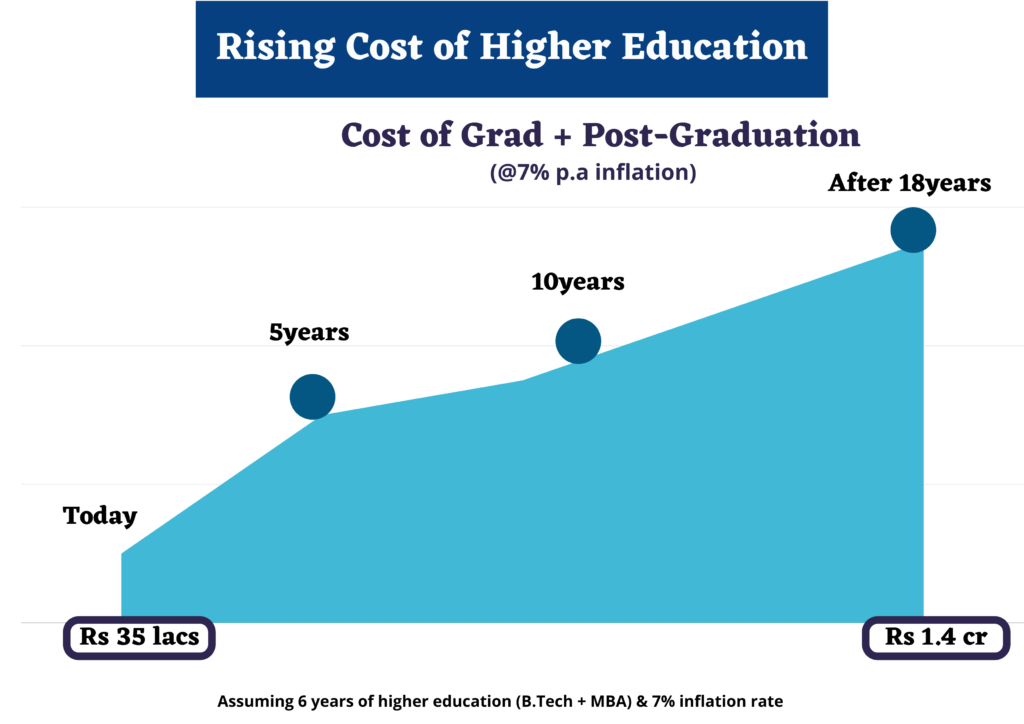

For instance, a fee for PGP course in IIM Ahmedabad was Rs11.5 lakhs in 2008 and today it is Rs 23 lakhs. Similarly, IIT (B.Tech) fees was Rs 2.28 lakhs in 2008 and today it is Rs 10 lakhs.

Can you see the exponential rate at which higher education costs are rising In India?

For students aspiring to get admission in foreign universities, the cost is almost 4 times excluding supplementary charges like accommodation, travelling etc.

Cost of education is rising at a much faster rate than inflation making it important for Indian parents to plan for child education. It’s not easy to fund your child’s education if you haven’t saved enough. Especially if you start planning late!

Let’s look at some of the mistakes made by parents which can be avoided easily.

5 mistakes to avoid in Child Education Planning:

- Underestimating the future cost of education:

Education costs is skyrocketing in India. A 4-year engineering course costs Rs.10 lakhs while a 2-year MBA degree can cost Rs 25 lakhs.

Effectively, a good higher education within India will cost more than 1 crore for a child born today assuming education inflation rate of 7%.

All this pertains to a domestic higher education. If you are looking to educate your child abroad, then the actual cost will be nearly 3 times this amount.

Be as aggressive as possible in putting down cost expectations.

2. Starting late:

It is very important to start early for success of child education planning. Ideally, start when you child is around 1 year old so that you have enough time at your disposal. The earlier you start, the more you save and, the more you save the more your money earns for you. This is referred to as the Power of Compounding.

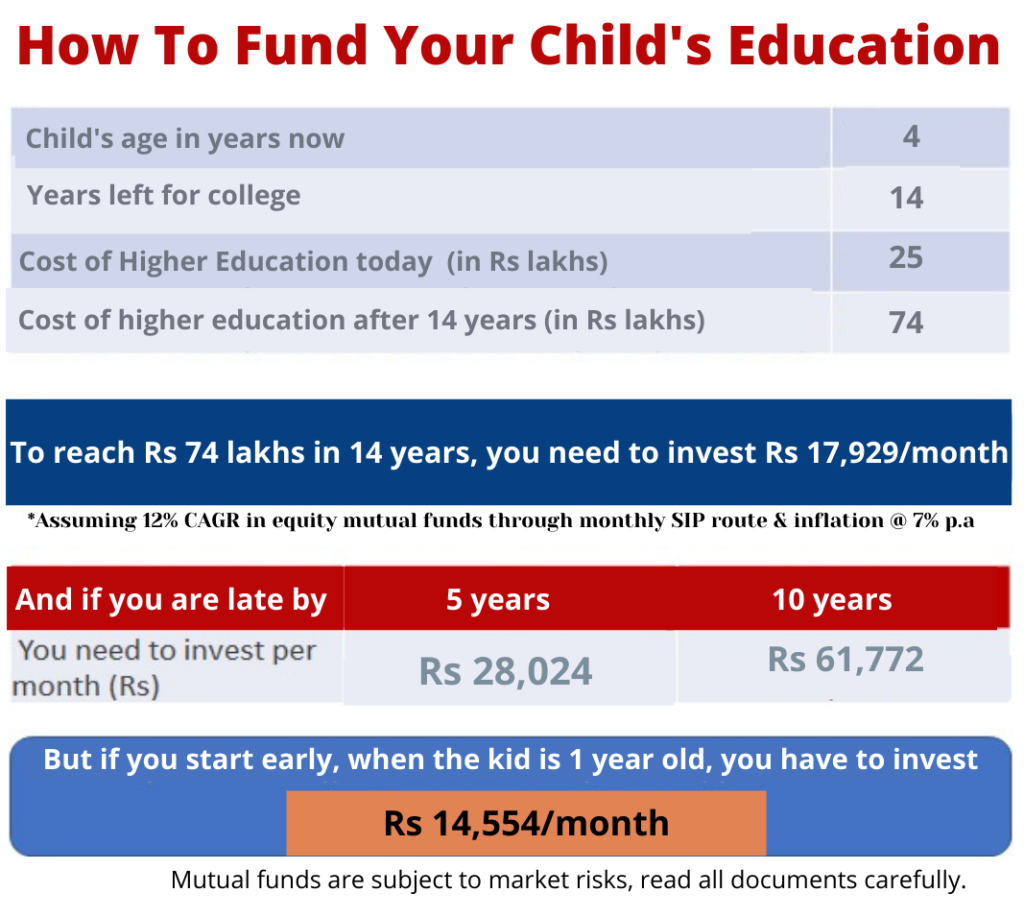

For example, if your child is currently 4 years old and currently the cost of higher education (Grad+post-grad) is Rs 25,00,000. Then the future cost of same education assuming 7% inflation rate will be Rs 74 lakhs and if you start investing today then the monthly SIP required to achieve the target is Rs 17,929.

However, if you delay your investments by 5 years or 10 years you will have to invest Rs. 28,024 or Rs. 61,772/month respectively.

But if you start investing when the kid is 1 year old, the required monthly SIP would only be Rs 14,554.

That is why starting early is so critical in child education planning.

3. Not investing in right products:

Never invest in assured but low return investment products/insurance policies. Don’t play it safe when it comes to planning over a 15-year period.

Equity and equity funds are best suited to outperform over the long term. Net Brokers believe that if you have a 15-year time frame there is no point in putting lot of money in debt. Look at investing at least 80% of your money in equity and equity funds to earn inflation beating returns. If you invest too much in debt, you are limiting your return generating capacity.

4. Ignoring regular review & rebalancing of investment portfolio:

Planning for your child’s future is not just about returns but also about managing risks. Diversify your portfolio and avoid exposure to sector funds for child education investment portfolio. Prefer the stability of diversified equity funds.

Net Brokers suggest to keep your investments dynamic and tweak the equity / debt mix as you go along. When you have 15 years to your child’s education it is fine to remain 80% in equities but not when the milestone is just 2 years away.

5. Relying on retirement corpus to fund child’s education:

Whatever the need may be, do not take money from the retirement corpus, or money kept for your other goals, for the purpose of your child’s education. Opt for education loan if there is a gap between amount saved for the education & the actual cost of education.

The most important thing to remember is that unlike your child’s education, you don’t have the option to avail of loans or receive any external assistance (such as scholarship or grants) to fund your retirement life. So, never touch your retirement corpus to finance your child’s education.

5 Things to do for right child education planning:

- Don’t ignore inflation:

Always plan for a higher level of inflation. It is best to keep it at 7% to 10%. Don’t assume less inflation.

- Plan your investments:

Start with child education planning as early as you can and invest the right amount in the right investment products.

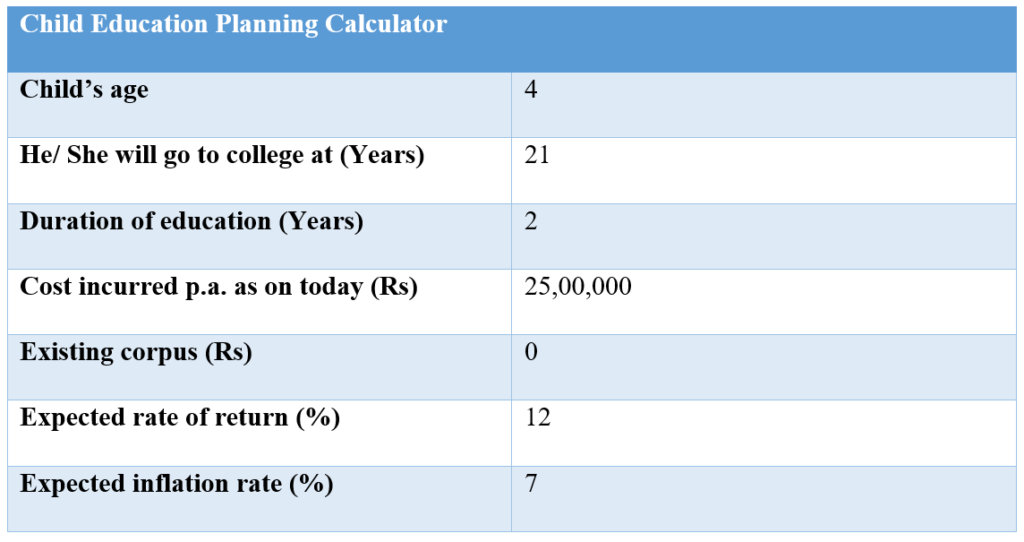

Use Net Brokers Child Education Calculator to fund out the future cost of your dream education. Let’s understand how child education calculator works:

Assume Mr Mohit wants his son, who is currently 4-year-old to complete his 2-year MBA from a premier foreign university which currently costs Rs 50,00,000. So, he starts preparing & planning to save for his son by entering his details in the child education calculator:

After filling the required details, child education calculator will give you the future cost of education and how much monthly you need to save to get the required corpus.

In this instance, Mr Mohit finds that the future cost of education in next 17 years will be Rs 1.6 crore and he needs to save Rs. 26,194 per month.

Download Net Brokers smart mutual funds app today and calculate the right amount that you need to start investing today to help secure your child’s future dreams!

3. Avoid lumpsum investment & invest via SIPs:

Lump sum investing is not a great idea for long-term goals. Rather start off with a systematic investment planning. With SIPs you can start early with small savings and reap advantages of power of compounding. And, you don’t have to worry about timing the market as the rupee coast averaging (RCA) takes care of beating the volatility & getting you the best price.

4. Step-up SIPs with rising income:

Our income increases over time. It may not happen in a linear fashion each year but on an average, it does increase. That means your approach to child plan investment must also be graded. Look to gradually increase your investments via SIP top-ups with rising income so that either you can use the funds for other purposes or you can get the corpus ready earlier.

5. Seek professional help:

There are plenty of investment options available in the market right now leaving investors confused about suitability of the product for their goals. In order to know how to save and invest and make the most of the different kinds of investment solutions, you can reach out to Net Brokers and take our help in picking the most suitable option matching your risk appetite & goals.

Net Brokers strongly suggest investors to start investment for child education at an early stage via monthly SIPs. This would ensure that investors reap the benefits of compounding in the long run.

Take the right step at the right time to make your child’s dream come true.

For more information, get in touch with us today! Download our mutual fund app & start investing for your long-term financial goals.

Happy investing!