Investors Guide to Mutual Fund Basics

By Akhil Chugh

Date April 1, 2021

Mutual Funds (MFs) have been a preferred mode of investment for a wide variety of investors for more than two decades now. MF investments in India have been ever increasing over the years but there are still huge opportunities awaiting owing to low MF penetration in our country.

If you are a new investor or an existing MF investor who is looking for answers regarding the working of MFs or clarification regarding its basic terminology then this article surely fits the bill. So do stay with us till the end and we guarantee you will be richer in your understanding of MFs.

Let us start with the basics of Mutual Funds and then move on.

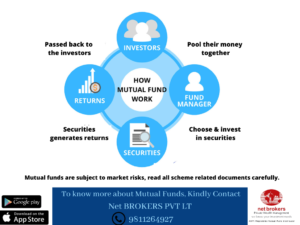

Working of a Mutual Fund:

A mutual fund collects money from investors having a similar investment objective into a common pool. The funds are then deployed to buy assets strictly in accordance to its investment strategy. For example, an equity mutual fund scheme will invest predominantly in a portfolio of stocks, while a debt fund will invest a significant portion of its assets in bonds. Within the asset class itself, the investment objective can be further sub classified to meet investor needs. Sector funds invest in companies belonging to particular sector and Large-cap Funds, Mid-cap Funds, etc., are focused on a specific market capitalization of stocks. To know about the best performing mutual funds in India, download our Net Brokers Mutual Fund app today.

Net Asset Value (NAV):

Investors are allotted units of the mutual fund scheme in lieu of their investment in the scheme. The price of these units is known as NAV (Net Asset Value) .Let us understand this concept with an example:

A mid cap mutual fund scheme collects Rs 10,000 each from 1000 investors, thus collecting Rs 1crore in total. Subsequently, it issues 10 lakh units with a NAV of Rs 10 each which are allotted to the investors in proportion to their investments.

The amount so collected is then deployed by the fund manager in adherence to the investment objective of the scheme (lets say in 20 mid cap companies).

After a year, assuming the stock price of these invested companies increases and takes the portfolio value from Rs 1 crore to Rs 1.3 crore, the NAV of the said scheme will go up to Rs 13 (Rs 1.3 crore/10 lakh units). So, the investor wealth rises by 30% from Rs 10 to Rs 13 in this case.

Advantages of investment in Mutual Funds:

- Professional help in investing

- Reduced portfolio risk due to diversification

- Convenience & cost-efficiency

- Principle of compounding works

- Multiple options to suit different risk-return profile

- MFs like ELSS also helps in tax savings

SIP vs Lumpsum Investing – Route to MFs Investments

While investing in Mutual Funds, investors have two modes of investment to choose from. First is, Lumpsum investment and the second is the Systematic Investment Plan (SIP). The SIP option is similar to opening a recurring deposit (RD) with a bank. Like in the RD, your SIP will deduct a fixed amount from your bank at specified intervals—usually every month. This promotes disciplined investing among investors and ensure regular investments even during difficult market periods. To know the required SIP amount to achieve your desired corpus, use our SIP calculators.

Benefits of SIPs:

- Inculcates financial discipline

- Rupee cost averaging – buy more units when market is low and less units when market is high

- Benefits from power of compounding

- Low minimum investment amount

- Long term wealth creation

- Helps in achieving financial goals

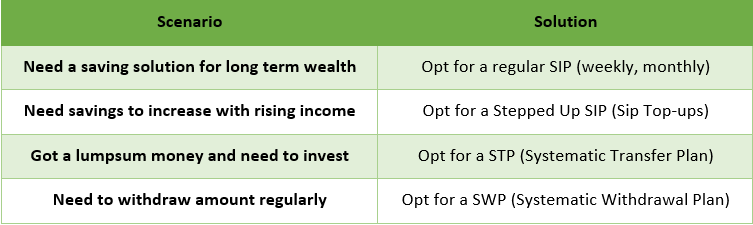

SIPs for all Situations:

Systematic Transfer Plan (STP):

Systematic Transfer Plan (STP) is also a type of investment route where an investor transfers a fixed amount of money from Source scheme to Target scheme (usually from a debt fund to an equity fund). STP is an excellent choice for investors looking to invest a lump sum amount, say a bonus or commission, but is not ready to do that at one go. This could be because they are risk-averse and do not want to get tangled in the market volatility. Such investors can opt to invest in liquid or debt funds (source funds). And can systematically transfer the fund to equity funds (target funds) over a period of time thus averaging their purchasing cost.

Systematic Withdrawals Plans (SWP):

SWP refers to Systematic Withdrawal Plan which allows an investor to withdraw a fixed or variable amount from his mutual fund scheme on a pre-defined date every month, quarterly, semi annually or annually as per his/ her needs. SWP is opposite of SIP, as in former you direct your investments from the plan to the savings bank account whereas in SIP, you channel your bank account savings into the preferred mutual fund scheme. Investors looking for income at periodical intervals usually use SWP to fund expenses during retirement.

In order to reap maximum benefit from mutual fund investments, it is important to diversify across different categories of funds. While anyone can invest in the securities market on their own, a mutual fund is a better choice for the only reason that all benefits come in a package. No matter how the market performs over the short-to-medium term, if your objective is to save for long-term goals, linking your SIPs to your long-term goals is the right step forward.

Start your SIP today with us, click here.

Happy Investing.