By Akhil Chugh

Date May 18th, 2026

We spend decades focusing on the accumulation phase of our financial journeys—religiously setting up SIPs, maximizing compounding, and watching our nest eggs grow. But very few people talk about the distribution phase.

Once you’ve built a solid corpus, how do you actually draw a substantial income from it without breaking your compounding engine or getting hit with a massive tax bill?

If you need a reliable cash flow of ₹1,00,000 per month to sustain your lifestyle, moving your entire corpus to a traditional Fixed Deposit (FD) might seem safe, but it is incredibly tax- inefficient and vulnerable to inflation. Instead, smart investors use an

SWP (Systematic Withdrawal Plan) to reverse-engineer their investments into a regular, tax- friendly paycheck.

What Exactly is an SWP?

Think of a Systematic Withdrawal Plan as an SIP in reverse.

With an SIP, you invest a fixed amount into a mutual fund every month to build wealth.

With an SWP, you withdraw a fixed amount from your accumulated mutual fund corpus every month to sustain your lifestyle.

The brilliant part? While you withdraw your monthly ₹1,0,000, the remainder of your multi- crore corpus stays invested in the market, continuing to generate returns and fighting off inflation.

The Mechanics:

How a ₹1,00,000 Monthly SWP Works

When you set up an SWP, you aren’t selling off your entire portfolio. You are instructing the fund house to redeem just enough mutual fund units to equal your ₹1,00,000 payout on a specific date each month.

Because the market fluctuates, the number of units deducted from your account changes based on the fund’s Net Asset Value (NAV).

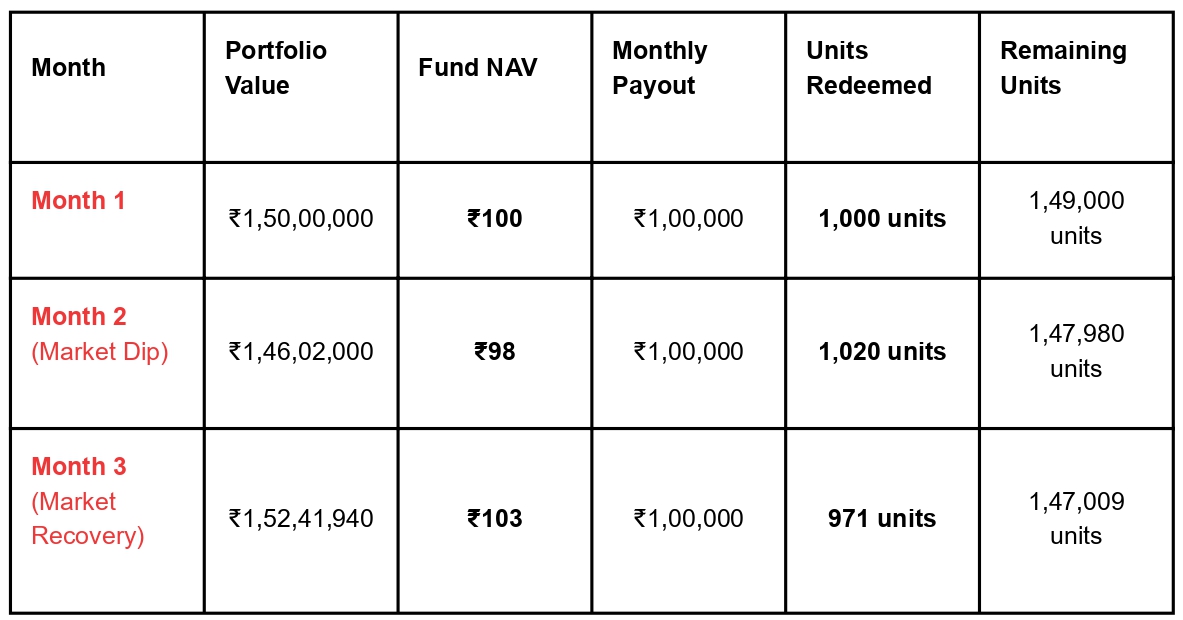

Let’s Look at the Data:

Imagine you have an accumulated mutual fund corpus of ₹1.5 Crores, and you set up a monthly SWP of ₹1,00,000. Here is how the unit redemption adjusts to market volatility over a three-month period:

- When the market is down (Month 2): The NAV drops to ₹98, so the system automatically redeems slightly more units (1,020) to ensure your ₹1,00,000 payout remains uninterrupted.

- When the market recovers (Month 3): The NAV jumps to ₹103, meaning fewer units (971) are sold.

This automated process removes human emotion from the equation, preventing you from panicking and selling off massive chunks of your portfolio during a market dip.

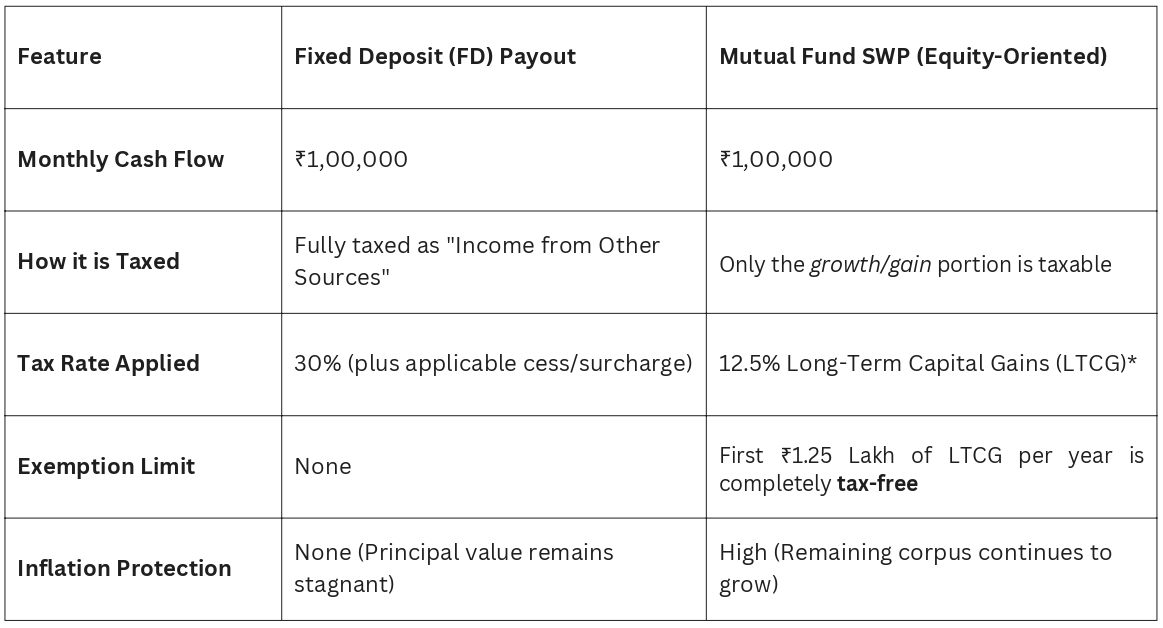

SWP vs. Fixed Deposit: The ₹1,00,000 Tax Showdown 🛡

Why choose an SWP over a traditional FD to get your monthly ₹1,0,000? It all comes down to how the government taxes your income.

If you are in the 30% tax slab and rely on FD interest to generate ₹12,000,000 a year (₹1,00,000/month), the entire interest amount is taxed according to your slab. You lose a massive chunk of your income straight to taxes.

An SWP payout, however, is treated as a redemption of capital gains. You only pay tax on the profit component of the ₹1,0,000, not the principal.

Comparative Breakdown (Assuming 30% Tax Slab):

*Note: Tax rates are based on current capital gains tax frameworks for equity-oriented assets held for over 12 months.

Because a significant portion of your monthly ₹1,00,000 withdrawal is simply your own original capital coming back to you, your actual tax liability drops drastically, leaving significantly more cash in your pocket.

The Golden Rule of SWP Sustainability

To ensure your money lasts throughout your lifetime, your withdrawal rate must be lower than the expected return rate of the fund.

For a ₹1,00,000 monthly withdrawal (₹12 Lakhs annually), a total corpus of ₹1.5 Crores represents an annual withdrawal rate of 8%. If your portfolio is structured to earn an average conservative return of 10% to 11% over the long term, your core corpus will not only remain intact—it will actually continue to grow, protecting your purchasing power against inflation.

Customizing Your Distribution Strategy

Transitioning from saving money to spending it requires a careful balancing act. You need to choose the right asset allocation—such as Hybrid, Balanced Advantage, or Equity Savings Funds—to minimize volatility while keeping your money working for you.

Ready to transition your portfolio into a reliable, tax-efficient income generator? Contact Net Brokers, your trusted mutual fund distributor, to map out a customized SWP strategy!