By Akhil Chugh

Date April 27th, 2026

As we approach the end of the first month of the new financial year, the most common sentiment in the market is “caution.” With the Nifty hovering at current valuations, many investors are sitting on the sidelines, waiting for a “clearer signal.”

But in wealth management, waiting is not a free option. It is a choice with a quantifiable cost. Today, we break down the three numbers that will define your portfolio’s success over the next decade.

1. The “Cost of Delay” (The 1-Year Penalty)

Many investors believe that entering the market 10% lower next year is better than entering today. The math suggests otherwise.

If you are 30 years away from retirement and miss just one year of compounding on a

₹50,000 monthly SIP (assuming a 12% CAGR), the terminal value of your wealth changes drastically:

- Starting Today: ₹15.40 Crores

- Starting 12 Months Late: ₹13.69 Crores

- The Difference: ₹1.71 Crores

To recover that ₹1.71 Crore “loss” caused by a 1-year delay, your future investments would need to generate an additional ~1.5% Alpha every single year for the next 29 years. Market timing is a gamble; time-in-the-market is physics.

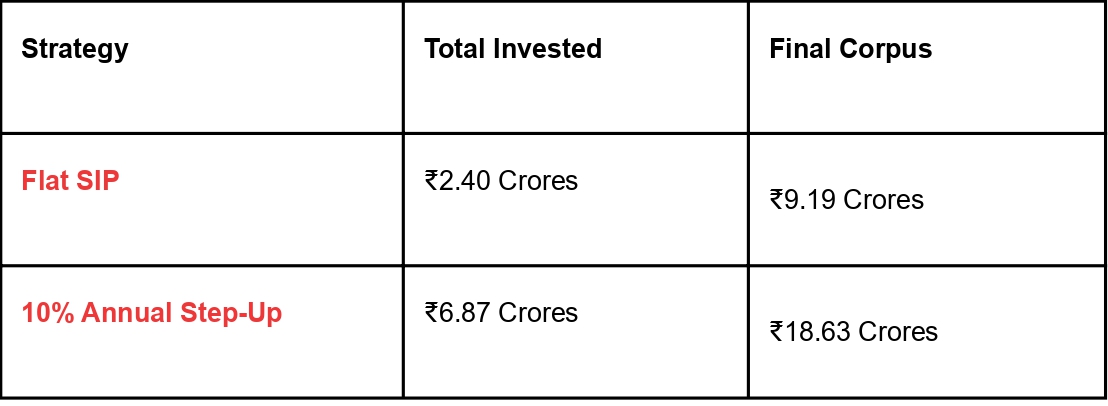

2. The Step-Up Multiplier:

Most investors treat their SIP as a “set and forget” tool. However, a flat SIP is a declining

asset when adjusted for lifestyle inflation.

Consider a ₹1,00,000 monthly investment over 20 years at 12% CAGR:

By simply increasing your contribution in line with your annual income growth (10%), you don’t just add 10% to your result—you nearly double your terminal wealth. In April 2026, the single most important click in your investment dashboard is the “Top-up” button.

3. The “Real” Return Reality Check

Wealth is not the number on your screen; it is your purchasing power. With core inflation holding steady, your “nominal” returns are deceptive.

If your fixed deposit offers a nominal return of 7% while inflation stands at 5.5%, the effective post-tax return for an individual in the 30% tax bracket reduces to approximately 4.9%. This translates into a negative real return of –0.6%, meaning your wealth is eroding in real terms despite the apparent growth.

To truly achieve financial independence, it is essential to allocate a significant portion of your portfolio toward inflation–beating assets. Equity mutual funds, with their potential to deliver a sustainable real growth rate of 6–7% or more, provide the long-term compounding power required to outpace inflation and build genuine wealth.

Money Monday Actionable Checklist

Before the market volatility of the week takes over, execute these data-driven moves:

- The 5% Rule: Audit your savings If you have more than 5% of your net worth sitting in a 3% savings account, you are losing purchasing power every hour. Move the surplus to a Liquid or Arbitrage fund.

- The Step-Up Audit: Ensure your SIPs for FY 2026-27 have been stepped up by at least 10% compared to last year.

The Final Word:

The market doesn’t reward those who predict the future; it rewards those who mathematically prepare for it.

Stay Disciplined. Invest Professionally. Stay Invested.