7 Mistakes to Avoid While Planning Your Child’s Education

By Akhil Chugh

Date July 6, 2025

Higher education is no longer just a dream – it’s a massive financial goal.

An undergraduate degree that costs ₹30 lakhs today could shoot up to over ₹1cr in 18 years, assuming an annual inflation of 7–8%. And that’s just the starting point. Add a master’s or overseas education, and the figures skyrocket.

That’s why early and informed children education planning is crucial.

But many parents make common mistakes that cost them dearly in the long run. In this blog, we break down the 7 most common mistakes – and show you how to avoid them using SIP calculators, smart strategies, and consistent investing.

Common Mistakes to Avoid While Planning for Your Child’s Education

Planning and investing wisely is no child’s play. Especially, when it comes to planning for your child’s future. In addition to making the right money decisions and opting for appropriate investing avenues, you also need to avoid some common mistakes as listed below:

1. Delaying the Investment

It is common for parents to get complacent and delay the investment process thinking there is ample time to invest. The perception that it is okay to start investing for your child’s future once he/she starts going to school is a prevalent and erroneous one. In the gamut of investments, time plays an extremely crucial role – the sooner you start saving and investing, the more time you will have for the power of compounding to allow it to work its magic on your money. It is very important to start early for success of child education planning.

For example, if your child is currently 4 years old and currently the cost of higher education (Grad+post-grad) is Rs 50,00,000. Then the future cost of same education assuming 7% inflation rate will be Rs 1.5cr. If you start investing today then the monthly SIP required to achieve the target is Rs 35,857 considering the expected CAGR of 12%.

However, if you delay your investments by 5 years or 10 years you will have to invest Rs. 56,048 or Rs. 1,23,544/month respectively.

But if you start investing when the kid is 1 year old, the required monthly SIP would only be Rs 29,108.

That is why starting early is so critical in child education planning.

Tip: The earlier you start, the lesser you need to invest monthly. Time is your biggest asset.

2. Underestimating Future Education Costs

Over the years, education costs have escalated quite a bit. According to rough estimates, on an annual basis the education inflation is about 10 percent p.a.

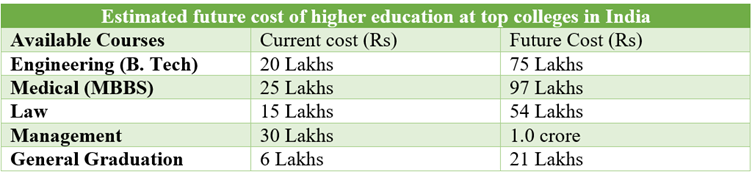

To estimate the size of the investment corpus required, let’s look at the cost of some popular courses in India at top institutes and assess their future cost 18 years from now, assuming the conservative inflation rate at 7% p.a.

Even by conservative estimate, if education cost inflation of 7 per cent a year is considered, then a 4-year engineering course that costs Rs 20 lakh at present will cost around Rs 75 lakh after 18 years. Similarly, a 2-year MBA course that costs around Rs 30 lakhs would cost around Rs 1.0 crore over the same time period. Here, we have considered the course fees for top colleges in India. The cost would be significantly higher (almost 4 times) if your education plan includes studying at a reputed foreign university.

Knowing the required corpus to finance your child’s higher education will help you understand the amount of savings that are required to be invested for child’s higher education.

Many parents tend to skip the intricacies of calculating the impact of inflation and the steep jump in education costs while estimating their target corpus. Hence it is crucial to figure out a realistic number and design an investment plan accordingly to ensure that you do not fall short of funds for your child’s education.

Tip: Use an education inflation calculator or get in touch with our experienced finance professionals and invest via SIPs accordingly.

3. Relying Only on Traditional Instruments

Never invest in assured but low return investment products/insurance policies. Don’t play it safe when it comes to planning over a 15-year period. Fixed deposits, PPF, and child insurance policies rarely beat inflation and won’t get you to ₹70 lakhs or ₹1 crore in 10–15 years.

Equity funds are best suited to outperform over the long term. Net Brokers believe that if you have a 15-year time frame there is no point in putting lot of money in debt. Look at investing at least 80% of your money in equity funds to earn inflation beating returns. If you invest too much in debt, you are limiting your return generating capacity.

Tip: Use mutual fund SIPs tailored to your time horizon and risk profile.

4. Ignoring regular review & rebalancing of investment portfolio:

Planning for your child’s future is not just about returns but also about managing risks. Diversify your portfolio and avoid exposure to sector funds for child education investment portfolio. Prefer the stability of diversified equity funds.

Net Brokers suggest to keep your investments dynamic and tweak the equity / debt mix as you go along. When you have 15 years to your child’s education it is fine to remain 80% in equities but not when the milestone is just 2 years away.

Tip: Review your portfolio annually and gradually reduce equity exposure as you near your goal.

5. Not having a term plan:

While planning and investing for your child’s future, one should not forget about life’s unpredictability. An unfortunate incident may leave your loved ones struggling to keep their finances afloat. Any working person with financial dependents should purchase a term insurance plan. Should anything happen to you, the payout from the plan can help your child continue their education.

A term plan’s sum assured should be at least 10-20 times your current annual income. Contact us to know more about available term insurance plans.

Tip: A term cover of at least 15–20 times your annual income provides a financial cushion, so your child’s education doesn’t get compromised—even in your absence.

6. Keeping SIP Amount Static:

Inflation grows, incomes grow – but if your SIP doesn’t grow, you’ll fall short.

SIP Simulation:

- ₹20,000/month SIP for 15 years = ₹1 crore

- ₹20,000/month SIP with 10% annual top-up = ₹1.55 crore

That’s ₹55 lakhs extra just by growing with your income!

Tip: Use a Top-Up SIP to increase your monthly investment by 10–15% every year.

7. Relying on retirement corpus to fund child’s education:

Whatever the need may be, do not take money from the retirement corpus, or money kept for your other goals, for the purpose of your child’s education. Opt for education loan if there is a gap between amount saved for the education & the actual cost of education.

The most important thing to remember is that unlike your child’s education, you don’t have the option to avail of loans or receive any external assistance (such as scholarship or grants) to fund your retirement life. So, never touch your retirement corpus to finance your child’s education.

Tip: Prioritize your retirement—your child can get a loan, you cannot.

Net Brokers Takeaways:

Education is the biggest investment in your child’s future – and planning for it isn’t optional anymore.

Start with child education planning as early as you can and invest the right amount in the right investment products. Download Net Brokers app and use SIP calculators, goal planners, and smart investing tools to secure your child’s dreams – whether it’s an IIT degree or an overseas MBA.

There are plenty of investment options available in the market right now leaving investors confused about suitability of the product for their goals. In order to know how to save and invest and make the most of the different kinds of investment solutions, you can reach out to Net Brokers and take our help in picking the most suitable option matching your risk appetite & goals.

Take the right step at the right time to make your child’s dream come true.

For more information, get in touch with us today! Download our mutual fund app & start investing for your long-term financial goals.

Stay invested.