How Mutual Funds Can Help You in Retirement Planning?

By Akhil Chugh

Date December 5th, 2021

Who doesn’t look forward to that golden period – free from work and family-related responsibilities? You have all the time to pursue your passions and live your dreams. But to be able to lead a comfortable life post-retirement, you need to have a significant retirement corpus as well as a steady source of income (pension). Failing to plan for your retirement now is planning to fail financially after retirement.

A recent survey found that the current generation of Retirees in India generally regretted not saving enough in life. Also, those who are now preparing for their retirement expect to save for at least 6 more years than their previous generation. Retirement Planning has become more crucial as Indian demographics depict a trend of higher life expectancy, an increase of nuclear families and absence of social security system.

We all have heard the famous story of the ant and the grasshopper. The grasshopper delayed storing food for winter, as it seemed too far away when the sun was shining nice and bright. And when the winter approached, he was left with no food & shelter to survive. Retirement planning could suffer a similar fate as we tend to prioritize near-term goals over it.

It is very important to realize that normal working life of any individual is till 60 years and assuming a life expectancy of 80 years, there is no income for the rest of the life. Therefore, we need to create a sufficient retirement corpus to last for these 20-25 years to live a stress-free retirement life and make the most out of it.

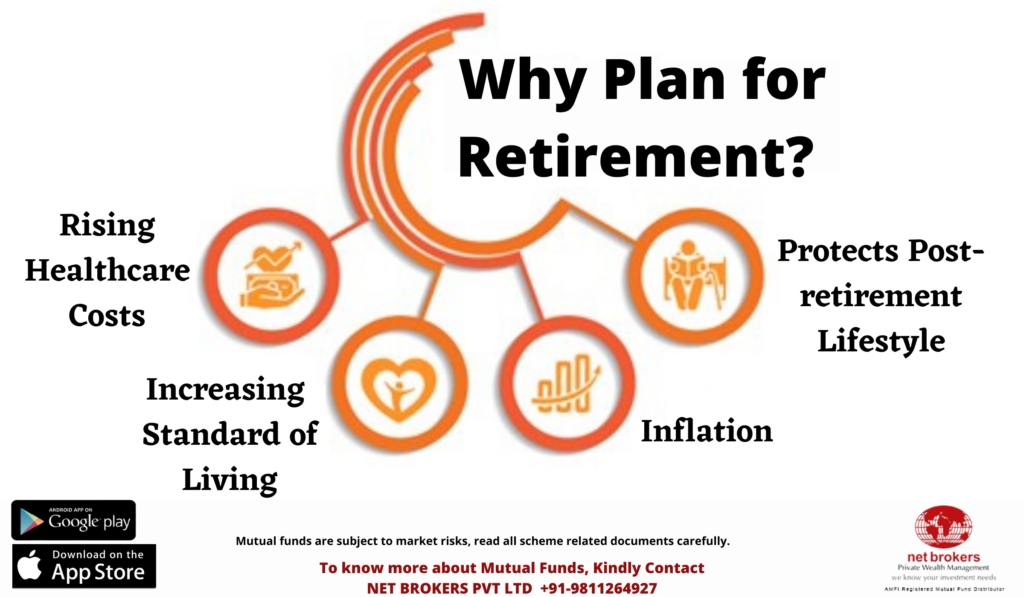

Key Reasons to Plan for Retirement:

1. Stress-free retirement Life:

Do you want to live a happy and peaceful life after your retirement – a phase when your monthly income is no longer coming into your account? The key to having a happy life post-retirement is to start investing as early as you can and have a retirement corpus in mind. You need to plan for a target retirement corpus that shall meet all your financial needs and goals in the future so that you don’t compromise on your lifestyle or quality of life at any stage.

2. No Social Security System:

India does not have a social security system like developed countries where the elderly is taken care of by the government.

3. Rising Healthcare Expenses:

With growing age, medical expenses usually account for the largest chunk of your total expenses. And this cost is sky-rocketing. The average medical inflation in India is around 12-14%, which is almost double the economic inflation in the country.

4. Rising Inflation:

The expected retail price inflation in India is 5.1% for 2021-22. This implies that a meal that costs you Rs 100 today, will cost you Rs 105.1 next year.

5. Increasing Life Expectancy:

Life expectancy in India is increasing every year with advancements in healthcare. Longer life means you’ll need more retirement funds saved to continue to live off. That means saving more and planning for longer. The earlier you begin, the better your chances are for having enough retirement funds to last your entire lifespan.

Benefits of Building Retirement Portfolio Via Mutual Funds

Mutual funds have emerged as one of the most popular asset classes to accumulate funds for various financial goals, one of which is retirement. Judicious planning coupled with prudent investment in mutual funds can help you build a sizable retirement corpus that can help you take care of your post-retirement needs with ease.

Here’s is a list of benefits of planning for your Retirement via mutual funds,

1. Flexibility:

Mutual funds are among the most flexible financial instruments available. They give you the flexibility to increase your investment with a rise in income via SIP top-ups and withdraw funds when required.

If you can track market movements, you can invest in mutual funds via lumpsum mode. For others, mutual funds provide a SIP mode of investment giving the dual benefit of rupee cost averaging and compounding. You can also switch from a poor-performing fund to a better one if needed.

2. Transparency:

The Securities and Exchange Board of India (SEBI), the regulator guiding mutual fund investment in the country, has introduced several measures to make mutual fund investment more transparent and investor-friendly. Steps like fund categorization and introducing the new risk-o-meter are aimed at making investing in mutual funds more transparent.

3. Tax-efficient:

Mutual funds are tax-efficient financial products as their post-tax returns are high compared to other financial instruments. Long-term capital gains (LTCG) from equity funds above INR 1 lakh are taxed at 10%.

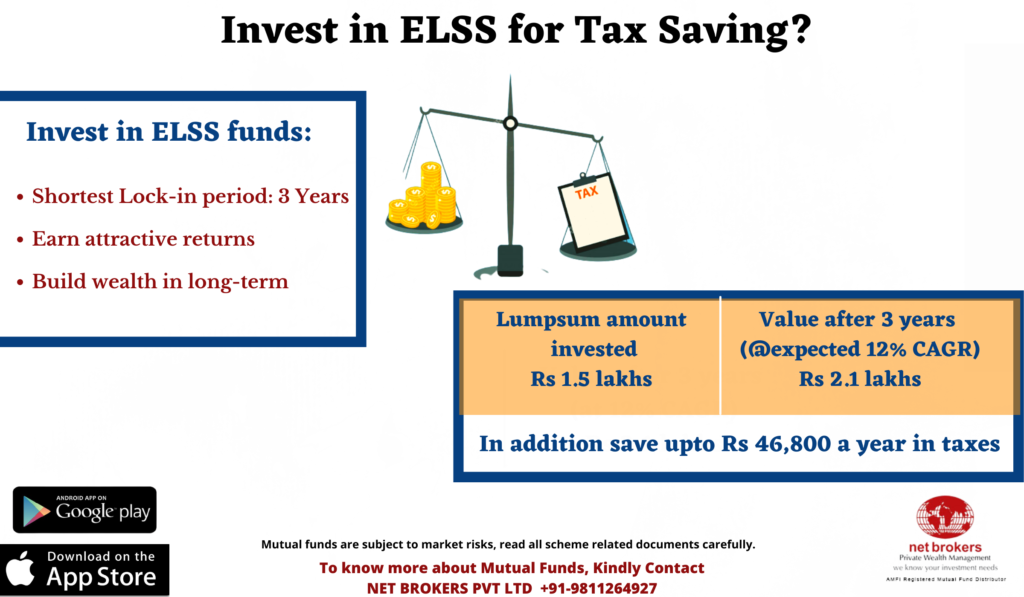

There is a class of equity funds known as Equity Linked Savings Schemes (ELSS) with a lock-in period of 3 years which is a tax-saving investment under Section 80C of the Income Tax Act, 1961. By investing in ELSS, you can claim a tax rebate of up to Rs 1,50,000 a year and save up to Rs 46,800 a year in taxes.

In the case of debt funds, 20% LTCG tax is levied after indexation which reduces the cost of acquisition thus bringing down the final tax amount.

4. Wide range of options:

The mutual fund universe is vast. You can invest in a range of funds as per your post-retirement needs. If you are starting early, you can opt for equity funds to build your retirement corpus. As you near your goal, you can shift from equities to debt to protect the gains from eroding due to market volatility.

5. Diversification

Diversification indicates building/ creating an investment portfolio that includes securities from different asset classes. It spreads risks across various financial investments, reducing the impact that poor returns from any one investment are likely to have on the overall portfolio.

Mutual funds are the easiest way to achieve diversification as well as asset allocation without in-depth knowledge of each asset class. By investing in mutual funds that invest in different asset classes such as equity, debt, and gold, you can spread your risk. Within each mutual fund category, investment is diversified across different sectors to balance risk and reward in the long run.

When to Start Planning for Retirement?

Today.

Retirement planning should ideally start from the day you start earning to reap the maximum benefit of compounding.

We usually delay retirement planning, because we follow an order of goals. For example, buying a car at 25 years of age is more important, owning a house at 35 years of age is more important than retirement planning & so on. However, the best choice for any early retirement plan is to begin investing in your early 20s. By doing this, you can accumulate a higher amount of corpus with a small amount of monthly investments.

Starting retirement planning early gives you an edge as with a longer investment horizon, the compound interest in your investments increases exponentially. This is the power of compounding.

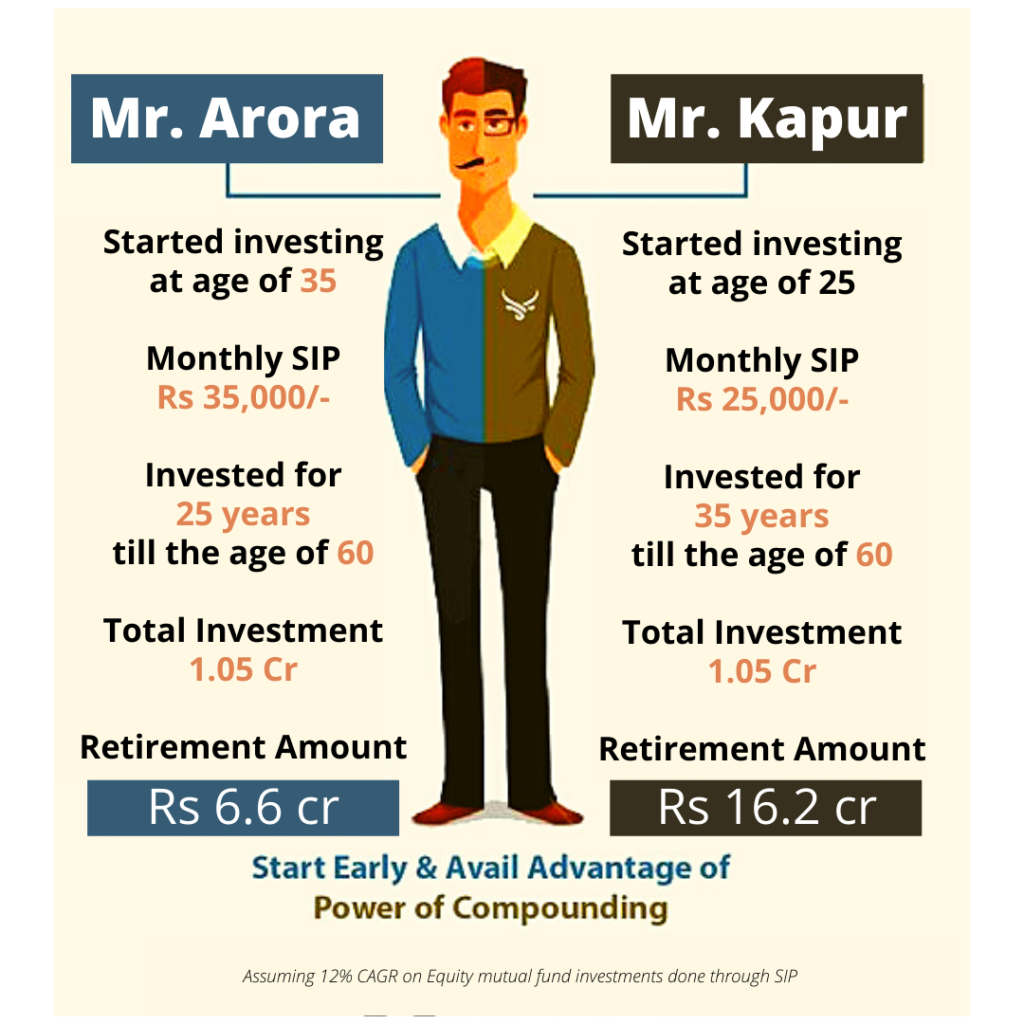

To help put things into perspective, here is a little representation of the impact of delaying investing.

Mr. Arora & Mr. Kapur are working professionals and are expected to retire at the age of 60. Mr. Kapur starts monthly SIPs of Rs 25,000 in equity mutual funds at the age of 25 years, giving him 35 years to accumulate the desired retirement corpus. On the other hand, Mr. Arora starts monthly SIPs of Rs 35,000 in equity mutual funds at age of 35 years, leaving him with 25 years of investment horizon to accumulate the corpus.

Let us assume that they both invest in an equity mutual fund with an expected return of 12% CAGR,

As evident from the above illustration, even though Mr. Arora invested (Total investments: Rs 1.05 crore) as much as Mr. Kapur (Total investments: Rs 1.05 crore), he could not accumulate a corpus anywhere close to Mr. Kapur because he started late. That is the cost of delaying and the magic of compounding!

Thus, starting early is crucial in retirement planning.

Key Takeaways from Net Brokers:

- A small amount invested for a long time period would fetch better returns than a one-time investment. It’s always better to start early to unlock the power of compounding to accumulate the desired retirement corpus.

- Never withdraw funds from your retirement corpus, before you have retired, irrespective of the financial emergency as you cannot avail of any loan from any source to fund your retirement life.

- Review & adjust your investment portfolio regularly to earn maximum returns.

- Have different plans for different goals such as retirement, child’s marriage, child’s education, etc. Never use funds that are intended for some specific purpose, when you need money.

- Start your retirement planning as early as possible via monthly SIPs in equity mutual funds. Equity mutual funds give returns that beat inflation over the long term and can help you accumulate a substantial retirement corpus to fulfil your retirement dreams.

- Invest regularly & increase your investments every year with rising income via SIP top-ups.

Net Brokers strongly believes that the right financial planning, while working, lays the foundation of your life after retirement. Do not go by hearsay in investing your hard-earned money, and instead, take the help of financial experts of Net Brokers to make prudent & right decisions for yourself.

Get in touch with us today to learn more about how you can successfully plan your retirement.

Download our mutual fund app & start investing for your long-term financial goals.

Happy Retirement Planning!