5 Things to do at the start of the financial year

By Akhil Chugh

Date April 3, 2022

A new financial year is an ideal time to start a new financial journey full of financial decisions driven by financial goals. It is a good time to review your investments and assess where you stand. This financial review will help you know how you have done with your finances in the last year, where you stand today, and the steps you need to take to have a successful financial journey to achieve your short-term and long-term goals.

In this blog, we have listed 5 key things to do at the start of the financial year 2022-23 to make it a better year for your investments.

1. Review your investment goals:

The start of the financial year is a perfect time to review your progress towards your goals. It is possible the target amount of your financial goals might have moved up more than you had assumed when calculating the amount, you will need. For example, if you were planning for a child’s education abroad, the dollar appreciation can make the foreign education expenses zoom up. In such a scenario, you will need to recalculate the SIP amount you will need to invest every month to have the required corpus to finance your child’s education.

Additionally, if there is a big change in your life stage in the last year like marriage or a child’s birth, you might have to rework the priority or add new goals.

2. Review your investment portfolio:

Though investing for the long-term is the ultimate key to wealth creation, that doesn’t mean you should invest and forget. A periodic review of your investment portfolio is essential, and the start of the financial year is a perfect time to do it.

A review will help you understand which funds have outperformed, which have performed in line with your expectations, and which funds have lagged behind. And while removing laggards is tempting, you need to be careful how you approach making that decision.

Ideally, you should only consider those funds which have been underperforming for more than 18 months. A clear definition of underperformance is crucial to making the right decision. A fund giving negative returns might not be underperforming if the entire category has fallen. So, you need to compare the fund performance vs. the industry average. For example, if the fund has fallen, but that fall is less than the industry average, then you might want to stick to it because of its superior downside protection capabilities.

Reviewing your portfolio is also useful when your goals change. For instance, you started investing in an Equity Fund when you were 10 to 15 years away from your retirement goal. But now, you have almost reached your target amount and are only two years away from your retirement. In such a scenario, you need to allocate a higher amount of this accumulated corpus to fixed income products via a systematic transfer plan (STP).

3. Review your insurance needs:

Major life events like marriage, becoming a parent, buying a house, etc., can increase your responsibilities significantly. You need to make sure that your life cover is sufficient to cover all these additional responsibilities.

So go back to the calculations you would have used to figure out the right cover for yourself, add the amount you will need to cover the additional responsibilities, and whatever extra cover you need, get that.

Ideally, your cover should be enough to provide a monthly income to your dependents, settle all liabilities, leaving enough for future one-time major expenses like the education of your children.

Similarly, review your health insurance needs as well. For instance, if you bought a policy before you get married, you would have bought an individual cover and for an amount that will be sufficient for you. Now with additional members in the family, you will need not only a more significant cover but also to make sure they are covered. The most convenient way to achieve this is by converting your health policy into a family floater and increasing the cover. This ensures continuity of the policy, and you don’t miss out on any benefits.

Contact Net Brokers to help you choose the right Term Plan and Health Insurance Plan based on your needs.

4. Increase your monthly investments:

Ideally, you should increase your SIP investment by 10% every financial year with a rise in your income by opting for SIP Top-up. This will help you reach your financial goals faster by fully leveraging the power of the compounding effect. SIP Top-ups can help you in syncing your investments with increasing income. It can automatically account for any inflation during the given time period. A SIP can help you buy your dream home soon, while a top-up could give you the leverage to buy it sooner.

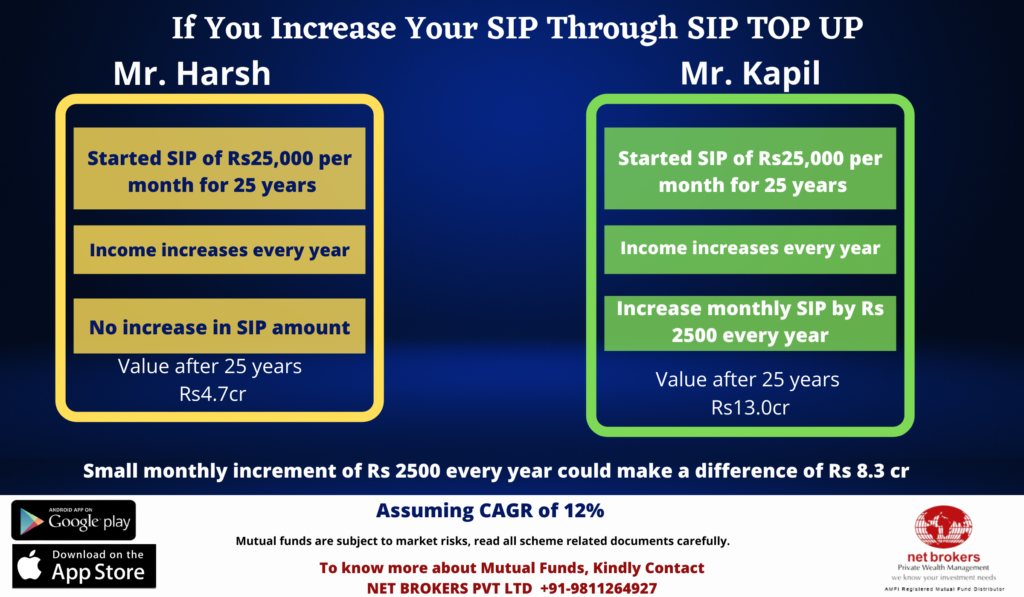

Suppose, Harsh & Kapil are two friends. They want to save money for their retirement which is due in 25 years. They decide to start a SIP in a chosen mutual fund scheme. Harsh decides to invest Rs 25,000 each month while Kapil opts for SIP Top-up and decides to invest Rs 25,000 per month with a monthly top-up of Rs 2500 every year.

Assuming a CAGR of 12% p.a., Harsh was able to accumulate Rs 4.7 crore at the end of 25 years while Kapil was able to accumulate Rs 13.0 crore at the end of the same time frame.

A small monthly increment of Rs 2500 made a difference of Rs 8.3 crore in their accumulated wealth!

Below is the graphical representation of two strategies:

5. Start your tax planning:

It is best to start your tax planning early in the financial year. That’s because you have enough time to calculate how much you need to invest to save the maximum tax possible and evaluate all options available. Since you have the entire year to invest the amount, you can spread these investments over the entire financial year.

Tax planning at the start of the year becomes all the more critical if you are going to invest in market-linked products like ELSS. Having a monthly SIP that helps you save tax over the year will ensure that you benefit from rupee cost averaging. On the other hand, if you wait till the last minute, you will have to invest even if the markets are at an all-time high and there is a possibility of them coming down. Planning for the beginning of the financial year not only saves you the chaos later but is also a smart financial decision.

The above are must-dos for every person to ensure a smooth year ahead. Net Brokers suggest its investors seek guidance from our team of financial experts to do goal-based planning & investments for you to help you achieve your desired goals.

Here’s to a wealthy Financial Year 2022-23!