5 Mistakes to Avoid When Investing Through SIPs

By Akhil Chugh

Date October 30, 2022

Mutual funds are a great way of investing in the stock markets for investors to create wealth in the long term and meet their financial goals. Mutual Funds carry relatively lower risk as compared to direct participation in the equities markets while generating comparable returns. This is because mutual funds are managed by professional managers and they have a diversified portfolio of securities to spread the risk around.

While investing in mutual funds, people can either opt for a lump sum or via SIP mode. For example, if you plan to invest a lumpsum amount of money, say Rs 10 lakh in mutual funds all in one go, this is a lump-sum investment. On the other hand, if you choose to make your investments in chunks, say Rs 20,000 per month for the next 10 years, then this is considered a systematic investment plan (SIP).

In general, the SIP mode can be a little more convenient way to invest in the equity market to create wealth in the long run. Some of the benefits of investing in mutual funds through SIPs are as below:

- Inculcates financial discipline

- Rupee cost averaging – makes market timing irrelevant

- Benefits from the power of compounding

- Helps in reaching financial goals efficiently

- Convenient mode of investment

But often, investors end up making mistakes that could lead them to losses or miscalculate the SIP amount or the target amount.

Here are 5 key SIP mistakes investors should avoid making to get the most out of their SIP investments.

5 Key Mistakes To Avoid When Investing in Mutual Funds Through SIPs:

1. Waiting for the right time to start Your SIP Investment:

A wise man once said, “the best time to plant a tree was twenty years ago; the second-best time is now.”

The same analogy may be applied to mutual fund investments as well. Instead of waiting for the right time, the present time needs to be considered as the best time to start SIP investments. This not only helps the investors to start investing in their financial goals at an early stage but also allows more time for the investors to reap the benefits of compounding in a better manner.

Investments grow over time. When one starts investing early, one gets a considerable head start over others in similar situations who start late. Compound interest was referred to by Einstein as the eighth wonder of the world and rightly so. Just like investing early gives a head start, it also brings with itself the wonderous compounding effect. However, even if you have a late start, regular investments can help in making up for the lost time if you keep on topping up your SIPs with rising income.

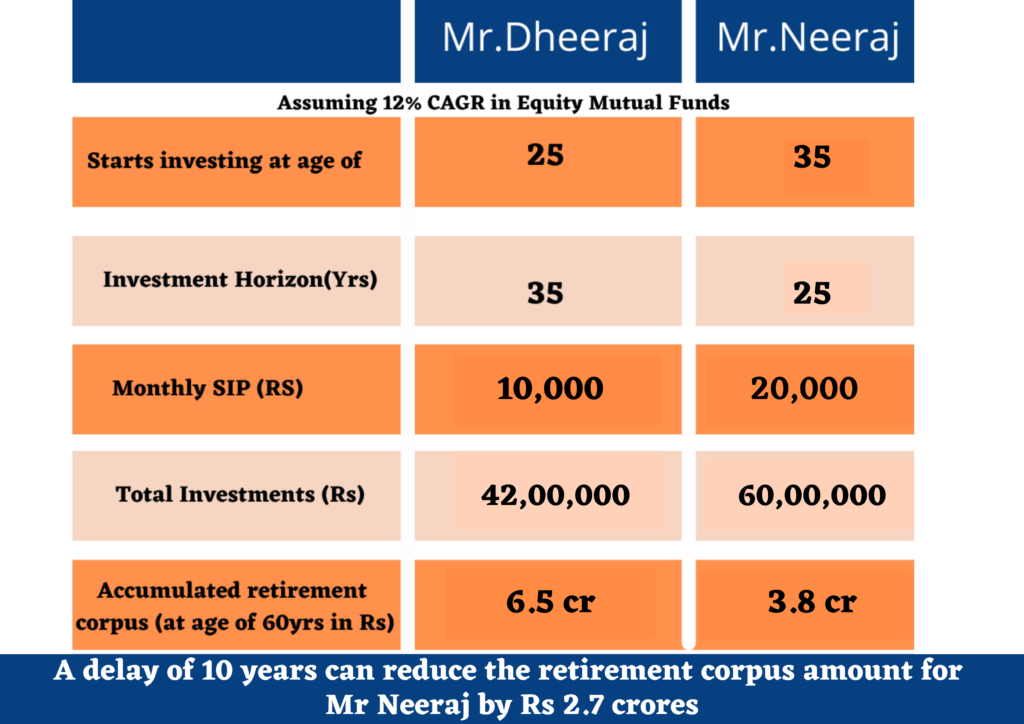

Let’s look at the illustration to understand how early investing is beneficial. Consider Mr. Dheeraj is 25 years old and Mr. Neeraj is 35 years old. Mr. Dheeraj starts his investment journey via monthly SIPs of Rs 10,000 in equity mutual funds at the age of 25. While Mr. Neeraj starts investing monthly SIPs of Rs 20,000 in the same equity mutual funds at the age of 35. Considering the 12% CAGR returns, at the retirement age of 60 years Mr. Dheeraj will be able to accumulate Rs 6.5 crores while Mr. Neeraj will only be able to accumulate approximately 1/2th of Mr. Dheeraj’s corpus i.e., Rs 3.8 crores.

This is the magic of compounding. In the investment world, time is your biggest friend. Time creates money. The earlier you start, the easier it is!

However, if Mr. Neeraj opts for an annual increment of Rs 830 then he would be able to accumulate the same amount of Rs 6.5 crores even if he starts late. To know more about SIP top-ups contact us today!

2. Stopping SIPs in volatile markets:

This is one of the most common mistakes investors make when starting SIP plans. Even though they start out with great enthusiasm, but little volatility in the equity market makes them stop their existing SIPs.

In simpler terms, this is another version of the investors trying to time the markets, by deciding against future investments to prevent further loss. However, the investors fail to realize that when the markets are falling or have already fallen, there is an exciting opportunity to invest at lower valuations and average the cost of investments. Further, stopping the existing SIPs may also pause the journey toward the achievement of financial goals and, thus, hamper the financial plans. Instead, the investors should believe in the long-term growth story of the markets and continue investing in mutual funds through SIPs.

Ignore the market movements when investing through SIPs to reap the benefit of rupee cost averaging and invest in the category of funds matching the investment tenure and your financial goals.

3. Not having goal-based SIPs:

Every individual has life goals that he needs to reach in the short term or long term. Calculating and investing regularly to be able to reach that financial goal is called goal-based investing. For example, if you plan a foreign holiday with your family in early 2023, which is 14 months away, it can be called a short-term goal. If you wish to plan for higher education for your child who is 8 years now, you have 10 years, and it is considered a medium-term goal. If you are 25 years old and have just started working and want to retire at 55, you have 30 years to plan for that goal and it is classified as a long-term goal.

So, it would be a massive mistake if you simply start one or two SIPs in mutual funds without linking it with any goal. Such an investment strategy is equivalent to taking a random train without knowing your destination.

Thus, you must link your SIPs to clearly defined goals (Goal-based SIPs) like retirement, child’s education, child’s wedding, foreign holiday, etc. Then you’ll know precisely how long the project will take, and you’ll be able to plan your SIP accordingly.

Also, you are more likely to continue your SIPs when you start them for specific goals. Because when you have a goal in mind, you are all the more motivated to continue your SIP. You know that you will never achieve your goals if you discontinue your SIPs midway.

4. Not increasing SIPs with rising income:

Starting a SIP at the early stage of your life with a small amount is a good habit as you couldn’t have afforded to invest or commit a large amount considering your income or salary. As you grow professionally, your salary also grows simultaneously so will be your financial goals or aspirations. Thus, it is essential to increase your SIPs with rising income.

SIP Top-ups is an option available to SIP investors wherein they can automatically increase their SIP contributions in the fund they are already investing in. As investor’s income grows with time, they are more likely to have more sum available for investments. SIP Top-ups allow these investors to increase the investment amount periodically.

Some of the benefits of SIP Top-ups are:

- Helps you reach your financial goals faster and you can expand your goals during the time

- Helps you in syncing your investments with increasing income

- Helps you to build a larger corpus

- Top Up automatically accounts for any inflation during the given time period

- A SIP can help you buy your dream home soon, while a top-up could give you the leverage to buy it sooner.

- Allows you to keep investing in an existing plan rather than the hassle of managing multiple SIPs with rising investible income.

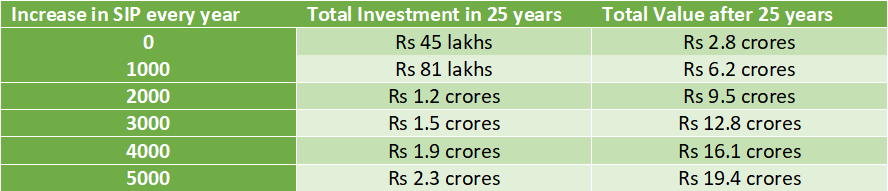

Let’s understand with an illustration how increasing SIP investments can make a huge difference. Suppose you started investing with a monthly SIP of Rs. 15,000. Assuming a CAGR of 12%, here is how different levels of increase in SIP investment every year will impact your total investment after 25 years.

As the table shows, if you increase the SIP amount every year, the amount you will earn is significantly higher than the amount you would earn if you continue with the SIP amount throughout your investment tenure.

In the above example, even as you are increasing only Rs. 3000 in the monthly SIP amount every year (20% of Rs. 15,000), the corpus you end up accumulating after 25 years is more than 4 times the amount you would have earned without increasing anything.

In other words, the opportunity you lose by not increasing SIP investments as and when your income goes up can be significant. Moreover, it will surely harm your overall wealth creation prospects in the long term.

5. Not reviewing SIPs performance periodically:

Starting SIP is just the beginning of your investment journey. It is not the end. So, you need to keep monitoring your investments in SIP against your long-term goals and see if they are in sync. Many investors start their SIP and later forget it completely. A lot many people have this misconception that long-term wealth creation means it doesn’t require monitoring at all.

To achieve your goals, it is important that you review your SIPs in different schemes once a year. The review will help you understand which mutual fund schemes have delivered as per your expectation and which schemes have underperformed. If a scheme has underperformed for 18-24 months, you can think of exiting that scheme. And if there is any change in portfolio’s total asset allocation, you can consider rebalancing the portfolio to align it with your risk tolerance and investment objective.

If the above-discussed mistakes are avoided and the goal, specifically, is well analysed and studied with the help of a financial expert, mutual funds could become a great mode of building long-term wealth.

Key Takeaways from Net Brokers:

- SIP in mutual funds is a great financial tool for investors as it not only avoids timing the market but facilitates them in their wealth-creation journey in a disciplined manner in the long run.

- While investing in SIPs, always think long-term. Stopping SIPs abruptly even if the market starts showing a bearish trend in a short duration is not a wise thing to do. The longer your investment horizon, the higher will be your scope to build wealth from the market.

- While deciding on the monthly SIP amount, assess your overall financial capabilities in the long run. If possible, opt for a plan that allows you to increase periodically the amount you invest.

- Seek professional help from Net Brokers to get the most out of your SIP investments as one wrong move can hamper your investment objectives and deter you from achieving your financial goals.

Starting SIPs early, continuing your SIPs, increasing SIPs periodically, monitoring SIPs on periodic intervals, and having SIPs for specific goals are some of the simple yet effective steps you can take to maximize your wealth creation. Make sure you follow these best practices to get the best out of your mutual fund SIPs.

For more information, get in touch with us today! Download our mutual fund app & start investing for your long-term financial goals.

Happy SIPs!